Analysis by Keith Rankin

New Zealand has a ‘fiscal responsibility’ clause in its Public Finance Act; a clause that began its life in 1994 as the Fiscal Responsibility Act. As a result, New Zealand has an effective ‘Balanced Budget policy’. A similar policy has been adopted this decade by the European Union (EU).

Balanced Budget policies are the single most important reason why the global financial crisis of 1929/30 became the Great Depression of the 1930s.

How do the world’s biggest economies manage their public finances, bearing in mind that their fiscal policies have global consequences?

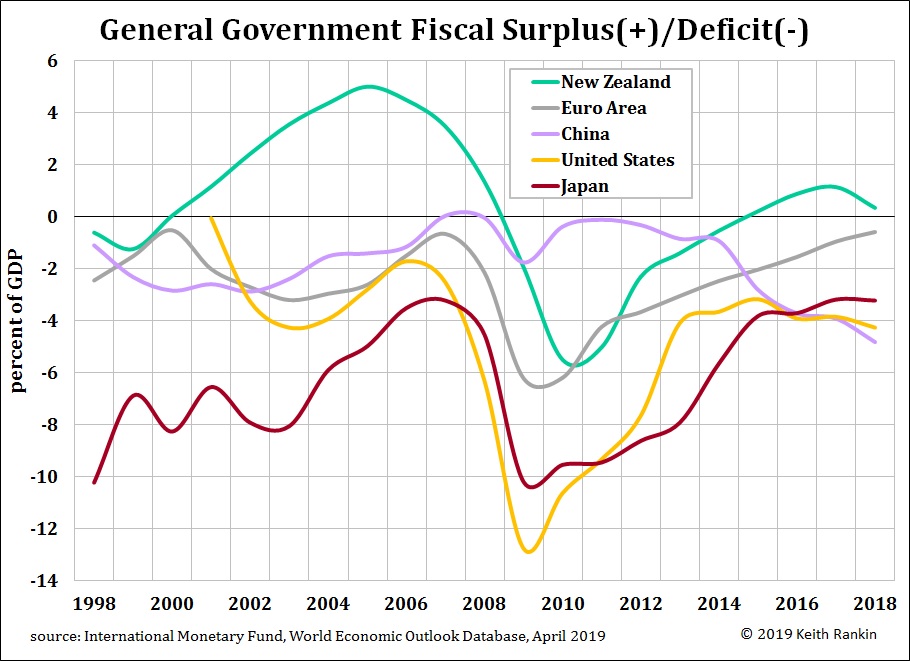

The United States and Japan have run structural deficits for decades. The last time Japan’s government sector had fiscal surpluses was for a few years around 1990, when its private sector was running amok in a brief debt-financed orgy of speculation. Financial conservativism (private) and pragmatism (public) has prevailed in Japan since then, with large public deficits offsetting equally-large private surpluses. Japan’s central government – and central bank – operate as debtors of last resort, maintaining economic stability there. Japan is our best example of a mature capitalist economy. In Japan, government deficits offset ingrained and ongoing private surpluses.

Since 2007, the United States fiscal profile has been almost exactly the same as Japan’s. It the new world fiscal order, large and ongoing government deficits maintain a degree of stability and order in the capitalist world. The difference between the USA and Japan is that the USA has had private sector deficits. The USA as a whole – private and public sectors – has run deficits that offset global structural surpluses in its ‘foreign sector’. To too many within the USA, however, this is seen as a national problem rather than as a global solution.

While countries such as Japan and the USA facilitated recovery from the 2008‑09 global financial crisis (GFC) by running larger than usual public sector deficits. It was China – and only China – which saved the world capitalist order by intending to run large government deficits. And, ironically, that intent meant that China’s actual public sector deficits were small.

By substantially increasing government balance sheets, China stimulated consumer spending in China and in the countries that exported large quantities of goods and services to China. As a result, China’s tax revenue increased to match its expanded government spending. So China’s government, by being most willing to apply fiscal stimulus (as planned and substantial Budget deficits) to the world economic crisis, rescued the world capitalist economy and balanced its Budget.

China’s governments balanced their Budgets through increased (ie not decreased) public spending.

The EU, on the other hand, now pursues fiscal policies, like New Zealand, that undermine the world capitalist order. While little New Zealand hardly matters on a world scale, if we imagine a capitalist world made up almost entirely of small countries with governments behaving like New Zealand’s, then global capitalism would be in a state of collapse.

Thus the EU fiscal policy of ongoing public sector austerity – especially as it applies to the Eurozone countries – represents the single biggest risk to the world capitalist order. The next crisis of world capitalism will come when the USA decides to emulate the EU, and when China decides not to mount another rescue mission.

For the next decade, I expect that China’s fiscal profile will look much like that of Japan and the USA, as it already has since 2015. As in Japan, China’s government will look to offset its own increasingly austere private sector. China’s role in saving the world economy after 2008 has not been properly acknowledged.

{kind=link}