Analysis by Keith Rankin.

Last week I looked at how, for modern day purposes, monetary policy started around 1750. It began with the departure from the presumption that money is wealth to the idea that money is a veil and that therefore wealth is something else. That was, in a sense, the beginning of political economy as a branch of philosophy, morphing into economics as a social science. In the then new (now ‘classical’) utilitarian view, wealth came to be seen as useful ‘product’ and money as a ‘veil’.

The liberal view arose that the best monetary policy was no-policy; that is, no policy beyond the steady coin production of each sovereign’s Royal Mint. While no longer the definition of wealth, across the capitalist world, money was understood as central (as a lubricant or a catalyst) to the workings of a self-regulating productive super-machine. Money came to be understood (correctly) as a technology – a flow technology – rather than as wealth itself. The mercantilist idea of money as wealth – and of gold or silver as money ‘to be made’ – never disappeared, however.

With that view of money as a lubricant in mind, we today can understand that a shortage of money is always going to be a bigger problem than a surfeit of money. (A car with an oil leak will eventually grind to a halt. A car with an overfilled sump, on the other hand, will still function; it will function near-to-perfectly if there is a place within the car to park the excess oil.)

This new laissez-faire view of monetary policy changed once it was realised that the mechanism didn’t work in practice as it did in theory. While it didn’t work for multiple reasons, there was a continuation of the pretence that it did work. In order to maintain that pretence, senior bankers and political leaders – the emerging ‘lords of finance’ – turned to interest-rate manipulation within the context of the ‘gold standard’.

Ultimately, what societies’ elites wanted was to have a form of ‘liquid’ wealth that they could store over time, and which would maintain (or even increase, through the ‘magic’ of compound interest) its purchasing power across time. The merchant capitalist mindset came to prevail over the realisations of progressive bankers and economists. The elite-classes still wanted a monetary policy which would operate as if mercantilism was true.

The elite-classes wanted money to come at a cost, so that they could be sure money would remain scarce. Gold and silver mining (and latterly crypto-currency mining) have been the primordial costs of commodity money. Interest rates would have to serve as the entry costs of modern ‘as if’ money.

Modern Monetary Theory

There is a known and substantially correct story in academia – albeit ‘heterodox’ academia – about money, monetary policy, and the relationship between public finance (fiscal policy) and money. It’s called Modern Monetary Theory or MMT. The conceptual relationship between OMT (orthodox monetary theory, though a better name might be PMT ‘prevalent monetary theory’, or even better LMN ‘liberal-mercantilist monetary narrative’) and MMT is akin to the relationship in the 1850s between miasma-theory and germ-theory in epidemiology. (Many people died of cholera in Europe and the Americas because the scientific establishment clung onto the miasma theory, despite the overwhelming and increasing weight of evidence to the contrary.) MMT dispenses with the requirement that money must enter into circulation at a cost; and disposes of the argument that the public and private sectors are each-other’s rivals.

I was fortunate to meet Randall Wray at an economics’ conference in Sydney in 2011, and found that he and his academic collaborators already had a well-developed theoretical framework which matched some statistical work I was doing at the time. I had been exposed to the work of Japanese/Taiwanese macroeconomist Richard Koo, and his studies of the Japanese structural recession of the 1990s and Japan’s recovery from that event. Of importance was Koo’s concept of a balance-sheet recession.

The central idea is that core money is public debt; a set of promises spent into circulation and backed by sovereign governments. A simple example of this is traditional coin money, made from bronze or silver or gold. In MMT, what gives the coin its value as a token of circulation is the depiction of the sovereign’s head, and not the amount of precious metal in the coin. A second example lies in the history of central banking, whereby the original three central banks (in Stockholm, Amsterdam, London – all in the seventeenth century) pioneered central banking through their roles as bankers to their governments; in particular, they managed their governments’ historical war debts. Those debts became private assets; and the core assets on these banks’ balance sheets.

These banks evolved to become bankers to the other banks as well as bankers to the state. Almost all the world’s central banks – ie Reserve Banks – are now publicly owned; they are very much part of the apparatus of the state. While governments sub-contract monetary policy to semi-independent central banks, MMT suggests that monetary policy is in reality undertaken by nations’ Treasuries. As a result of Treasuries’ monetary misunderstandings, modern capitalism risks becoming like an under-lubricated car with leaks.

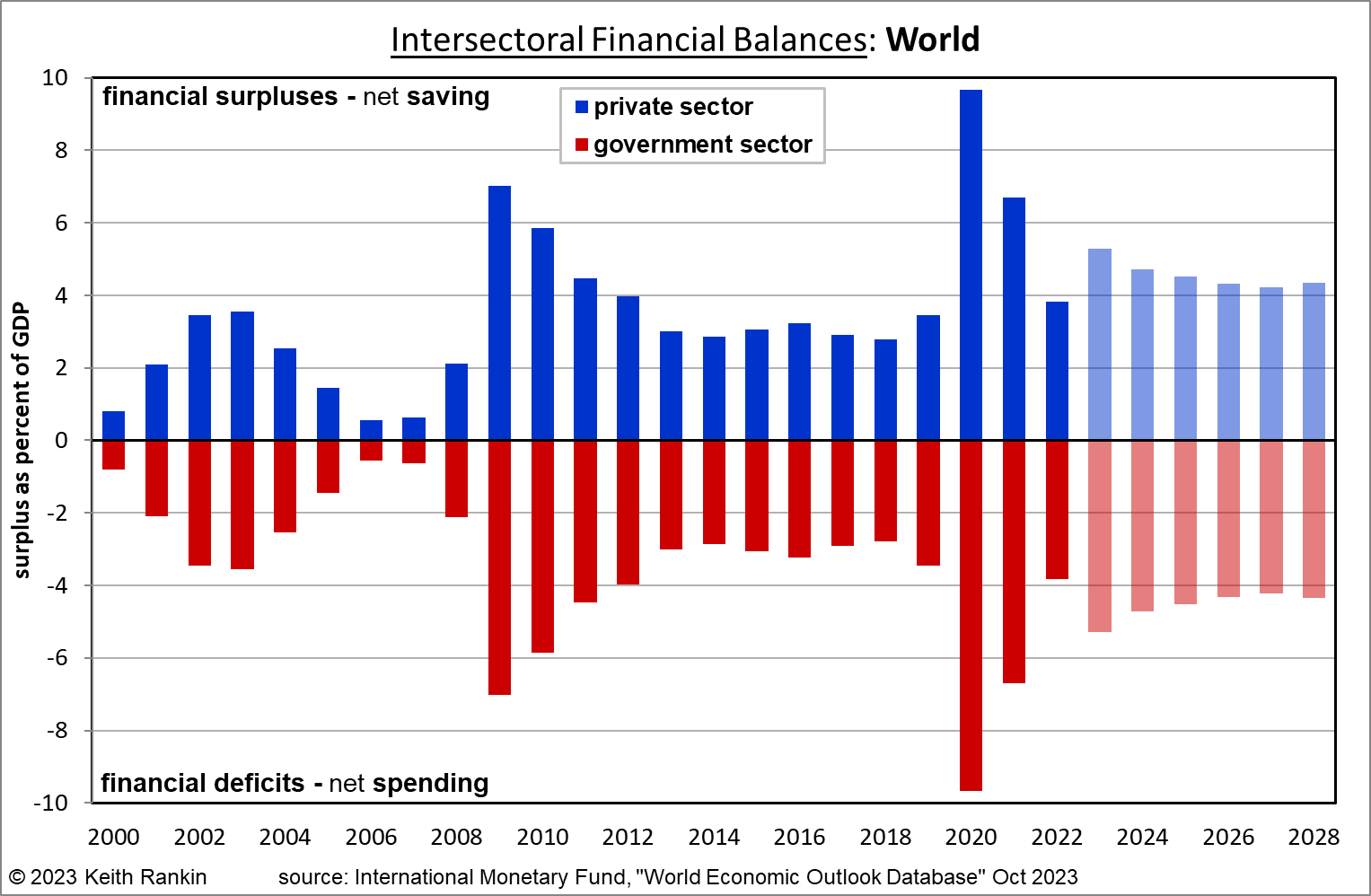

Public debt(s) are private assets, just as a bar of gold is an asset. The world’s effectual money supply is the ‘liquid’ – ie flowing or circulating – component of (or derivative of) any monetizable asset; the core monetizable asset being public debt. This chart (from my Governments run financial deficits; it’s their role to do so, Evening Report, 17 October 2023) shows that, this century, public debt – the monetary base – increased each year from 2008 to 2022 by an average of about four percent of global GDP. That’s about how it should be, and with significantly larger injections of money required whenever a financial or economic crisis threatens to undermine the circulation of money in the real economy, as occurred in 2008 and 2020.

The real economy is the purchases of goods and services. The ‘unreal economy’, into which much money leaks, is the ‘casino economy’ whereby money is spent on financial assets; non-money circulating promises such as shares, bonds, and property titles. The ‘upstairs’ casino economy acts as a dynamic treasure hoard, fuelled by leaks from the real economy, with players buying and selling assets at mostly increasing prices.

While according to MMT, public debt (not gold or silver) is the foundation rather than the pariah of capitalism, that is not to say that more public debt is always better than less public debt; just as, in the classical schema, more gold is not necessarily better than less gold. Though in 2025 Aotearoa New Zealand, more public debt would certainly be better than the present constricted amount. The growth of public debt is always limited by tax revenue arising from the circulation of money; as they say, nothing is more certain than taxes. One efficient way to increase public debt – and thereby enhance the liquidity of the economic machine – is through ‘negative income taxes’; for example, universal tax credits (which should act like the credits received in the game Monopoly whenever a player passes ‘Go’).

The prices of money

There are three important prices associated with money: the internal price (which wavers with pure inflation and pure deflation, and does reflect the idea of money ‘as if’ it’s a commodity like silver); the external price (the exchange rate between one form of money and another, eg $NZ vis-à-vis £UK); and the interest rate which is best understood as the price of ‘inter-temporal trade’ (although OMT treats it as the ‘necessary cost of money’).

Inter-temporal trade simply means exchanges when, unlike direct barter, selling and buying do not occur simultaneously. Wage workers effectively sell their labour on pay-day, and buy stuff (say at the supermarket) on another day. When they ‘save’, then it may be months or years before they spend that saved money; that is, months or years before they use it to buy stuff. Alternatively, workers may spend some of their wages in advance; for example, with a payday loan or a credit card. Interest rates are a market-clearing price which – if correctly set in the money market – ensures the balancing of income spent late with income spent early.

People who tend to spend their money before payday are usually net payers of interest. Likewise, people who spend most of their money after payday are net receivers of interest. Thus, interest rates should be high when few people want to spend late and many want to spend early; and low when many people want to save and few want to borrow. There is no reason why interest rates cannot be very low; that is, negative.

Negative real interest rates are indeed commonplace; they occur when the rate of inflation is higher than the interest rate. For example, if the internal price of money is falling by five percent a year (ie annual inflation is five percent) and the interest rate is three percent, then the real interest rate is minus two percent. Under such conditions, interest effectively flows from savers to borrowers; rewarding early spenders over late spenders.

(For a while in the late 2010s, Switzerland had a published interest rate of minus three-quarters of a percent and inflation at minus one-and-a-quarter percent, meaning that the real rate of interest was plushalf a percent. Everything worked fine; interest effectively flowed from borrowers to savers. Switzerland then needed negative interest rates in order to limit the appreciation of its currency the Swiss Franc; otherwise, the external price of Swiss money would have been rising too much. In that episode, all three prices of money came into play.)

Looking at the three prices of money dispassionately, we see that they all play a role in free market capitalism, and that the inflation rate is itself a part of the price mechanism. This indeed has been grudgingly accepted by the mainstream, with today’s monetary policy proposing the optimum annual inflation rate as two percent rather than zero; and there are advocates today for higher inflation targets. The internal price of money should fall, policymakers agree, albeit in a predictable manner. Australia indeed has a higher inflation target than New Zealand.

(If inflation is 2.1% every year for 100 years, two $20 notes put under the mattress today should buy one loaf of bread in the year 2125; $40 would become equivalent to today’s $5.)

One important benefit of inflation is that it encourages the circulation rather than the hoarding of money. The biggest danger arising from large caches of non-circulating money is that such money may reactivate at short notice, creating substantial ‘excess-demand’. Just as we are used to seeing money regularly leaking into the casino, money in the casino can be injected into the real economy at short notice.

Bimetallism as a way of favouring Inflation over Deflation

An early attempt at monetary reform during the gold-standard period was the advocacy of bimetallism.

The United States election of 1896 was fought, in effect, on the issue of inflation versus deflation. At that time, due to gold scarcity, the gold to silver exchange rate was high (16:1) and rising. There was a substantial world depression in the early 1890s; an event that hit Australia very hard, causing New Zealand to resist overtures to join the incipient Australian federation.

In the world of the gold standard, prices were at an all-time-low and many small businesses had become distressed; especially farmers who were selling their produce at prices which were falling even faster. In the United States the free silver movement was prominent, and the Democrat Party chose a candidate – William Jennings Bryan – who favoured that political position. He failed to get elected because there was an effective party split, with many urban voters in opposition to the policy to shift from the gold standard. (As a result of the Democrat split, many Gold Democrats aka Bourbon Democrats voted Republican. The new Republican president was the recently hyped imperialist William McKinley. The gold-silver exchange-rate issue largely dissipated following the 1897 Alaska gold rush.)

The anticipated effect of a switch to a silver or bimetallic standard was that prices and wages would go up, and the highly indebted small businesses would be able to service their debts in an environment of inflation rather than deflation. City workers in 1896 tended to favour deflation; many were unable to make the connection between their future standard of living and the retention of a thriving small-business sector.

As we have seen, this position of favouring inflation over deflation is now mandatory in most capitalist jurisdictions. The largely successful monetary policy attempts in the 2010s to ward-off deflation ensured that there was no general depression in that decade. The policy, strictly, was largely unsuccessful in achieving its inflation target. That’s because of one of the fundamental flaws in orthodox monetary policy; low interest rates generate lower rather than higher costs, and therefore low rates of CPI-inflation.

Examples of ineffective and effective monetary policy from (mainly) New Zealand history

There were antecedents of MMT (and other pragmatic initiatives) in New Zealand and elsewhere during the recovery from the Great Depression which peaked in the early 1930s.

In the 1920s New Zealand had no Reserve Bank. New Zealand’s (mainly Australian-owned) banks did their banking in London, the world’s pre-eminent financial sector. From 1926 until 1928, New Zealand’s Minister of Finance was William Downie Stewart, an economic liberal and a monetary conservative. Gordon Coates – more of a pragmatist, but largely untested – had been endorsed as Prime Minister in the 1925 election months after the death of William Massey.

1927 was a disaster year for New Zealand, exacerbated by Stewart’s unresponsiveness in his role. Australia had its economic meltdown a year after New Zealand, reversing the trans-Tasman migration flow. This made the government even less popular, as unemployment in 1928 was blamed on immigrants. Coates’ Reform Party – the principal precursor of today’s National Party – went from 48% of the vote in 1925 to 35% in 1928, losing power as a result. In 1929 there was a United minority government, initially facilitated by Labour. The winning policy of United – the former Liberal Party – was increased government borrowing. The result was 20 months, in 1929 and 1930, of relatively good times despite the unfolding international crisis.

Reform went into the December 1931 election as junior partner in a United-Reform Coalition (a formal coalition which formed that September). While gaining many more votes and seats that election than United, Reform remained the junior partner. Stewart was restored to Minister of Finance at the worst possible time; going into 1932, the most difficult year of the Great Depression. Labour’s doctrinaire socialism was unappealing to voters, despite the growing unpopularity of the United government in the months following the retirement and death of Prime Minister and Finance Minister Joseph Ward.

As a ‘sound-money’ man, Stewart had been a stickler for the revised gold-standard rules. However, before the 1931 election, Britain’s government collapsed due to the financial crisis. Britain had to suddenly withdraw from the Gold Standard. The ensuing rapid depreciation of the British pound (largely reversing deflation in that country) kick-started the British economy, and also brought the New Zealand economy out of its 1931 ‘free-fall’. But New Zealand, being an agricultural commodity economy facing severe terms-of-trade issues, needed an even bigger (and longer-lasting) currency reset. Eventually, in January 1933, Stewart did the right thing and resigned on a matter of monetary principle. Coates – Stewart’s replacement – now pragmatic and worldly-wise, immediately devalued the New Zealand pound against the British pound, in line with the recommendations of the young generation of economists.

New Zealand’s recovery remained slow, but at least it was under way. The management of New Zealand’s financial reserves in London remained too conservative. Nevertheless, many subsequently iconic new businesses began their lives in 1934 and 1935 (for example Wattie’s, Fisher and Paykel, Sleepyhead).

Coates did two more things of great importance. First, he established a reform-minded Brains Trust made up of three young economists – Campbell, Sutch, Belshaw – who would argue for monetary pragmatism. And Coates established the Reserve Bank of New Zealand in 1934. Though created with conservative monetary principles in mind, the means had become available to introduce heterodox monetary policy in the event of a future government willing to flirt with an alternative narrative.

Another important development was the rise in the United Kingdom in the 1920s of Social Credit, then known as Douglas Credit, a ‘lay’ movement (counter to the political economy traditions of Marshall and Marx) reminiscent of the previously-mentioned American ‘free silver’ movement. Social Credit largely antagonised academic economists, by making anti-orthodoxy generalisations which were simplistic and too broad. Nevertheless, Social Credit gained a substantial political influence, not least in New Zealand; and it did have policy prescriptions helpful for extracting economies from a state of structural recession and inequality.

In the Labour Government elected in 1935, there was a substantial Social Credit faction; and there were a range of other monetary reformers with varying degrees of sympathy towards Social Credit. Social Credit’s central argument was that the orthodox monetary system had a permanent and structural deflationary bias, and that a public institution – such as an appropriately modified central bank – would be required to offset this bias. In effect, Social Credit argued for quantitative easing, and a national dividend (and food price subsidies, called ‘compensated prices’) as means to inject new money into circulation while addressing monetary poverty and inequality. (See A National Dividend vs. a Basic Income – Similarities and Differences, by Oliver Heydorn, 2016.)

Unlike the quasi-Marxian form of socialism advocated by New Zealand Labour from the 1910s until 1933, the party under the leadership of Michael Joseph Savage became infused with monetary radicalism and a desire to unite rather than divide diverse economic interests.

A commitment to monetary reform within Labour in 1935 led many rural voters to vote Labour for the first time ever (including voting for my great-aunt’s husband in Kaiapoi). Those voters remained loyal to Labour in 1938, in light of Labour’s subsequent monetary achievements. Particularly effective was the State Housing programme, politically managed by John A Lee, a working-class monetary reformer. Labour made full use of the new Reserve Bank to create-through-spending the money required. Economic growth boomed (about 25% in two years) while inflation remained low; a big recovery from a big depression.

In New Zealand, Social Credit split from Labour in the 1940s, and formed its own political party. While often polling highly, it could not break the two-party system, and was eventually broken as a political force – in 1984 losing two-thirds of its 1981 vote – after having been lampooned by Bob Jones. Jones was leader of the one-election-wonder New Zealand Party; an ‘unsuccessful’ party which successfully acted as a political catalyst for the return of economic liberalism and the floating-currency version of classical monetary orthodoxy.

While much of what Social Credit claimed as chronic weaknesses of the orthodox monetary narrative has turned out to be true, the successful albeit piecemeal monetary reforms which took place in the middle-third of the twentieth century eventually undermined Social Credit’s critique of monetary orthodoxy. Social Credit had indeed contributed to its own seeming redundancy as an economic force in New Zealand. (There was a Royal Commission on Money in 1954, in which Social Credit had a chance to make a substantial case. Although there had been a near-recession around 1953, after the Korean War, and Social Credit gained 10% of the vote in 1954, there was little evidence then of structurally unsound monetary arrangements.)

A third important development was the publication in 1936 of The General Theory of Employment, Interest and Money by John Maynard Keynes, an already famous British economist. This was a largely technical book which extended and reconsidered Keynes’ earlier views on money and monetary policy (1930 A Treatise on Money), while emphasising the critical roles of public debt and government spending in getting a country out of structural recession. Keynes also recognised in 1933 that import protection through tariffs would help with national economic recoveries, and that national economic recoveries would enable the restoration of the international capitalist economy. Keynes criticised international capitalism in order to save it.

Keynesian analysis led to the pushing a string critique of monetary policy.

It was the Keynesian critique which created the post-war international expansion; underpinned by an emphasis on government spending as a curative for the kinds of unemployment which widely prevailed in the 1930s. But Keynes believed that the problem of the 1930s was more cyclical than structural; hence he argued – in contrast to the MMT argument – that governments should run budget surpluses during periods of full-employment.

Keynes was the architect for the post-war monetary system that might have been. But the alternative American-led version won out, with politics prevailing over good argument, and with Keynes’ premature death.

Keynesian and other insights from the Great Depression of the 1930s informed monetary policy during the global decolonisation period from 1946 to 1976. Newly independent countries emerged, all with central banks. Central banks became, more explicitly than before, an arm of government. In New Zealand, with its substantial historical national debt (a result of imports exceeding exports for around 100 years) the development of import-substituting and export industries became central to economic policy. Interest rates remained below the rate of inflation through sufficient costless money creation. Organisations close to government – especially the producer boards such as the Dairy Board, forerunner of Fonterra; also, the State Advances Corporation which funded mortgages – gained direct lines to practically costless money through their Reserve Bank accounts.

While those monetary reforms worked in their time, future fiscal-monetary policies will need to be more about sustainability and private-choice than through a single-focus on selling more goods in a stormy world marketplace.

Unfortunately, monetary policy from the 1980s regressed into the spirit of 1920s’ economic liberalism and monetary conservatism. The result has been the nonsense of simultaneous economic growth and deteriorating living standards through stagnant wages, overwork, unaffordable housing, and weak environmental stewardship; the inequality norm of the neoliberal era matches that of the early twentieth century.

Money is inherently public. Unfortunately, there is a ‘groupthink’ in the economics profession; the profession which describes economies with a very limited vision of capitalism’s public sphere. Modern monetary theory straddles capitalism’s public-private interface.

Financial Mercantilism and Labour Mercantilism

In the neoliberal counter-revolution of the 1980s, the Reserve Bank of New Zealand was mandated to use interest rates as a weapon to suppress inflation by creating a recession. Although government debt was costless to create, governments were obliged to pay high ‘market’ rates to borrow. A new ‘expensive-money’ era of neoliberal-mercantilism was born, in which money was required to have innate scarcity value. Money reverted to its former status as a commodity to be made and stored.

The neoliberal era is best characterised as a new period of financial mercantilism; an era in which money is king, and the objective of economic life is – through capital or through toil – to ‘make money’.

This neoliberalisation took an unusual path in New Zealand, in that the figure after whom these changes were identified – called ‘Rogernomics’, after Labour Minister of Finance, Roger Douglas – had a deeply set philosophy which can best be described as ‘labour mercantilism’. The philosophy dates to conservative working-class practices in the Victorian era, the Fabian era, and which gave a nod to Marxian class consciousness. In that era of working-class self-help, worker welfare came through worker-funded contributory societies in which all contributors had an equal stake and expected equal benefits, though spread out over time. To be a beneficiary, you had to be a contributor to the fund from which you and your family expected to benefit. Money earned in one period would be paid out much later. Pension-fund benefits, for example, paid out of saved money, needed to purchase new goods and services. While this idea presumes economic growth through the accumulation of physical capital, the initial withdrawal of money from circulation could inhibit such growth.

This funding idea forms the basis of ‘savings-funded’ pension schemes, as distinct from ‘pay-as-you-go’ taxation-based schemes. The savings-funded schemes create huge financial liabilities which must be liquidated in an inherently uncertain future; the fiction is that wealth is stored in the past to be consumed in the future. The current-tax-funded schemes, on the other hand operate entirely in the present tense; a person’s pension is determined by today’s economic conditions, not yesterday’s conditions.

Financial mercantilism is a ‘store-money-today’, spend it decades later perspective. Labour mercantilism is the variation applied to the savings of wage and salary earners.

In the late-1930s’ Labour Government there were three factions, which Michael Joseph Savage (Prime Minister) had to manage. There were the monetary radicals – the radical centre – which included Social Credit. There were the left-wing redistributors, who wanted to ‘tax the rich’ and ‘pay pensions and tax concessions’ to workers. And there were the ‘right-of-the-party’ labour mercantilists who wanted to withdraw money today to build sovereign wealth funds from which future retirement and other benefits would be paid to workers’ families. These last two groups squabbled intensively behind the scenes. (A very useful source is the 1980 book, The Politics of Social Security, by Elizabeth Hanson; another is A Civilised Community, 1998, by Margaret McClure).

That first Labour caucus included Bill Anderton, Roger Douglas’s maternal grandfather (MP for Eden and then Auckland Central from 1935 to 1960; no relation to Jim Anderton, whose father’s surname was Byrne and mother’s birth-surname was Savage, though no relation to Michael Joseph Savage). From 1960 to 1975, Norman Douglas succeeded his father-in-law Bill Anderton as MP for Auckland Central. Norman and Roger Douglas were in Parliament together from 1969 to 1975.

In 1937 there was a push from Labour’s right to abandon the 1935 policy pledge of universal pensions (and other benefits) in favour of an actuarial scheme – what we would today call a sovereign wealth fund – that was conceived-of as a kind of ‘magic money tree’ based on the ‘principal of compound interest’. Minister of Finance Walter Nash, returning from the United Kingdom in 1937, was accompanied by accomplished British actuary George Henry Maddex. Much time was spent with Maddex – some would say wasted – trying to supplant the promised ‘pay-as-you-go’ universal pension with this scheme which promised some people – mainly men – with large benefits in the distant twilights of their lives. Further, because the people who financially contributed the most would get the most, the scheme in essence promised an avalanche of future-spending by people other than those with the most needs. In the end the left and right factions cancelled out, resulting in a universal welfare state funded for current beneficiaries with current money.

Compound interest only works if interest is less than inflation over the medium-long term. In practice such ‘pension funds’ play about for decades in the casino economy, trying to replicate the promise of compound interest. Further, they represent capitalism’s greatest financial risk; the possibility that financial assets, dynamically-parked in the casino of capital gains, will sometime in the future return at scale and at short notice to the real economy. Flooding the future economy with excess demand. Or eventually providing deferred benefits which would buy much less than promised.

Fast forward to 1974, Roger Douglas devised and established such a sovereign wealth fund, which commenced operation in 1975, and was cancelled months later. In the midst of high inflation and a global economic crisis, the greater monetary priority was addressing the issues of that time, not stashing away stocks of money for the never-never. The National Party under Robert Muldoon fully exploited that misplaced priority.

When in power again in 1985, Douglas turned to the redistributive face of Labour, means-testing the ‘universal superannuation’ which had existed in one form or other since 1940.

Nevertheless, still alive and well at 88 – and long-after he established New Zealand’s most right-wing party, ACT – Roger Douglas is still pushing for the same sovereign wealth fund that his grandfather wanted in 1937 and that briefly operated fifty years ago. This time he has University of Auckland Economics’ Professor Robert MacCulloch at his side, claiming this pension fund as a magic bullet solution to New Zealand’s present stagnation (refer GDP drop sparks calls for Willis to step aside, RNZ, 19 Sep 2025). One-again, withdrawals from the ‘circular-flow of money’ will not rejuvenate an economy which desperately needs injections of ‘money-in-circulation’.

Kwasi-nomics

An interesting recent episode was the Fall 2022 rise and fall of Liz Truss as United Kingdom Prime Minister, and her hapless Chancellor of the Exchequer Kwasi Kwarteng. Truss and Kwarteng were right-wing monetary mavericks, willing to expand the United Kingdom’s public debt through ‘unfunded’ tax cuts. Yet the structure of those tax cuts was principally to allow the already rich to become richer, rather than to inject the money into where it was most needed. Subsequent to her effective dismissal, she went on to laud Argentina’s hatchet (aka chainsaw) President Javier Milei whose modus operandi is to drain money from those sections of Argentine society which most need it. Kwarteng and Truss were co-authors of Britannia Unchained, which argued ‘for a radical shrinking of the welfare state in order “to return it to the contributory principle … that you get benefits in return for contributions”. That’s the same quasi-economic principle which underpins labour mercantilism.

Ricardian Equivalence

Ricardian Equivalence is an idea gleaned from classical macroeconomics which became fashionable within neoconservative economics in the 1980s. It claims that fiscal policy is futile; that increases in government spending are ‘internalised’ in such a way that private spenders adjust by spending less. It has been widely used as an argument for the futility (rather than the centrality) of government spending as an engine to establish a healthy full-employment market economy.

Neoconservatives push the liberal-mercantilist monetary narrative as the only valid macroeconomic policy programme. Ricardian Equivalence, much-touted by economic liberals to justify fiscal conservatism, puts all their policy eggs into monetary policy. Meaning the monetary policy, based on innate money scarcity, of using interest rates to recreate the primordial costs previously associated with gold and silver mining.

Ricardian Equivalence is a ‘straw man’ argument. In as much as the data supports it, that conservative characterisation of government spending does not apply to economies stuck in depressions or structural recessions. Only programmes of active government spending – or waiting for too long – can resolve a structural recession.

And the monetary system always requires enough public debt to act as the banking-system’s ‘modern gold’.

Finally

Modern Monetary Theory is a valid description of money as it actually is (and was), and a policy recipe for economic growth. There are important twenty-first century stories which require money to be something more; in particular, a means to generate higher living standards and productivity without requiring economic growth. This is partly an issue of work-life balance, better enabling those who wish to choose more leisure and less work. And a prosperous future without economic expansion will be a requirement of a future of demographic contraction, as is forecast for the end of this century.

To achieve these ends, we have to go beyond public-debt-induced peoples’ money to achieve ways in which ordinary people – households of people who consume goods and services among other things – can choose their own balances between consumption and other facets of good living.

It can be done. Public equity dividends – dividends arising from public domain capital, equal and unconditional, complementing private incomes – can enable the overworked to work less and the underworked to work more. That could be the future direction of modern money.

*******

Keith Rankin (keith at rankin dot nz), trained as an economic historian, is a retired lecturer in Economics and Statistics. He lives in Auckland, New Zealand.

{kind=link}

{kind=link}