Analysis by Keith Rankin.

While our traditional economic indicators all seem positive and on target, it is nevertheless clear to almost everyone that something is very wrong with the economic health of New Zealand and other liberal-capitalist economies. Far too many people – especially young people – are poor. Many are trapped in their poverty. While some show trappings of affluence – thanks to their parents who provide housing and other amenities – they have little reliable income of their own.

There are three essential reasons for high levels of poverty and precarity in rich economies, two of which relate to the acquisitive behaviour of the rich; the top ten percent. These two causes – Causes Two and Three – manifest among those affected as a personal debt crisis and/or a rental housing crisis.

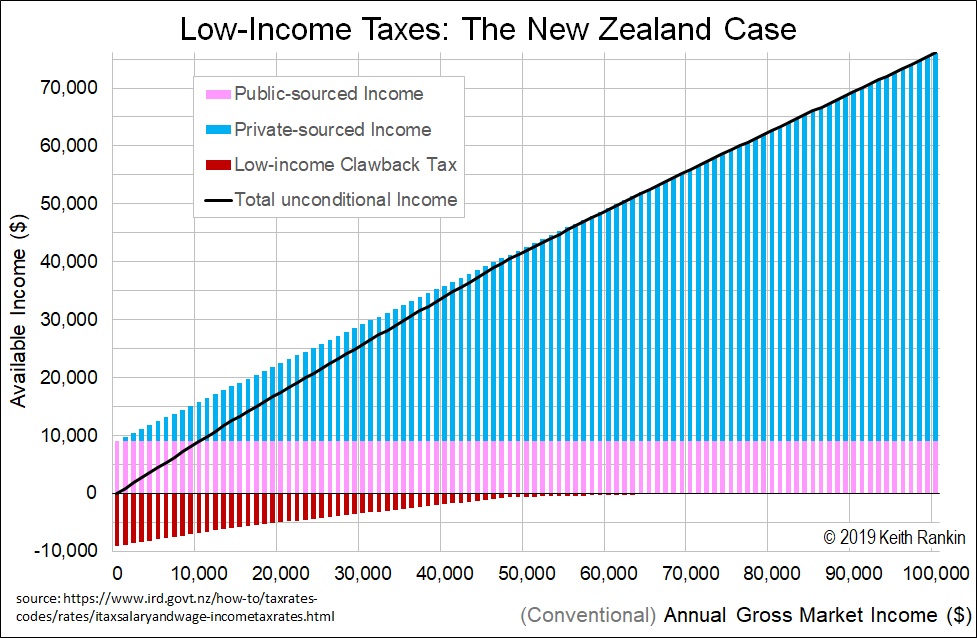

Cause One – which this month’s Chart reveals – is the confiscation of income that low‑income people face. In the Chart it is listed as “Clawback Tax”.

Most of us do not know about clawback taxes because liberal-capitalist societies are stubbornly wedded to unprincipled modes of public‑bookkeeping which conceal the underlying reality, rather than reveal it.

To appreciate the issue, we may go back to a brief debate that took place in New Zealand’s 2017 election campaign; the debate about who owns water. The previously unwritten convention (as enunciated by former Prime Minister, John Key) was that nobody owns water. The principled truth, it turned out, was that everybody owns water.

Water is one of the many resources in the public domain that serve as inputs into the market economy, the outputs of which are called gross domestic product (GDP). The standard (principled) convention of the marketplace is that businesses pay for their inputs (as costs). Thus businesses pay wages to their workers and rents to their landlords. But for some reason, we presume that businesses to not pay rents for their public domain inputs. Bookkeeping conventions pretend that all public domain inputs – including water – are free.

Public domain inputs are not free, and we do pay for them. The rent we pay for public domain inputs is called income tax (which includes company tax, and the PAYE personal income tax which is has been deducted at source in New Zealand since 1958). If, in the future, public domain inputs (such as technological knowledge) further diminish the labour contribution to GDP, then the rate of rent payable for public domain inputs should increase. The present underlying rate of income tax in New Zealand is 33 percent. That is the rental charge the New Zealand economy, since 1988, has paid for these inputs.

Principled public bookkeeping follows the principle that everyone owns public domain inputs, which include water, infrastructure, technology, social capital, and public institutions. And that, in New Zealand, 33 percent of GDP is the present rental charge on these inputs.

Applying these principles, we can say that any worker in New Zealand who would today say they earn $100,000 per year (what they would call gross personal income’, even though for an employee, income tax is deducted before that person receives it, on the basis that taxed income is public income, not the employee’s income) really earns $67,000 as personal private income (plotted in blue). In addition, such workers – as economic citizens, as holders of public equity – receive $9,080 as a dividend from the public income pool (plotted in purple). The result is that such workers end up with $76,080 of personal income available for spending. The right‑hand side of the Chart shows this for a worker grossing $100,000.

Likewise, for a person grossing $70,000 per year. Such a person has privately‑sourced earnings of $46,900 (67% of $70,000) and a dividend ($9,080) from the public pool. Total is $55,980. Again, this is shown on the Chart.

However, people grossing less than $70,000 are subject to a clawback tax. Consider a person grossing $50,000 per year. 67 percent of $50,000 is $33,500 (blue). The dividend from the public pool is $9,080 (purple). These add to $42,580. However, such workers incur a clawback of $600 (red in the Chart), leaving an available personal income of $41,980 (shown as the thick black line).

If we come down to a person grossing $20,000, their clawback tax is exactly $5,000. And a person with a gross market income of zero has their entire personal income ($9,080) clawed back. The public dividend is their only non‑transfer income, and it is entirely confiscated.

Because of this situation – the confiscatory taxation of the poor – we have poverty, serious income poverty.

We try to deal with this socially‑inflicted problem in various bureaucratic ways; mainly by giving conditional transfer payments (popularly called ‘benefits’ or ‘tax credits’), a student loan living allowances, and retirement pensions. For many the transfer is more – in monetary terms – than the clawback tax. But not for all. And in the case of students receiving ‘loan’ living allowances, the compensatory payment must be paid back in later years.

From the Chart, the most obvious policy measure is to remove the clawback tax. This is the one single policy measure that can liberate our young adults in particular from the fetters that keep them ‘at home’; the fetters that hold them back from advancing into responsible adulthood; the fetters that aggravate and in some cases initiate mental illness.

In cases where existing benefits do not fully compensate, governments will face a fiscal outlay. In many of these cases the fiscal cost will be very small. In the many other cases, there would be no fiscal cost. Rather the status of beneficiaries’ benefits would change, with the first $9,080 of existing benefits becoming transparently visible as those persons’ unconditional public dividends.

The first law of holes says that, to get out of a hole, a person should stop digging. Likewise, in dealing with low‑income poverty, the first thing our societies should do is stop confiscating low incomes through clawback taxes. Low‑income persons need to be substantially freed up to live their lives, both because unconfiscated income itself relieves poverty, and because victims of income‑poverty will be able to spend much less time applying to bureaucrats for compensation.