Analysis by Keith Rankin.

The Financial Profile of a Nation State

New Zealand Incorporated (in abbreviation, NZ Inc.) is Aotearoa New Zealand thought of as an economic nation. The domestic economy of New Zealand splits into the ‘Government’ and ‘Private’ sectors, where ‘Private’ means ‘non-Government’. ‘NZ Inc.’ is embodied within ‘World Inc.’; that is, within the ‘global economy’. From the point of view of a single country such as New Zealand, the rest of the world is called the ‘Foreign’ sector.

Financial balancing is a ‘zero-sum game’. Sectoral balances must total to zero; they must ‘balance’. This is because every dollar spent by somebody is received as revenue by somebody else, maybe by someone in another sector. If we consider revenue as a positive number (eg +$5) the associated spend by someone else is the equivalent negative number (in this case, -$5). Further, every dollar lent by someone is borrowed by someone else.

Each country (as an ‘incorporated’ nation) can be understood as a three-sector economy: G(overnment), P(rivate), F(oreign). A positive balance for any sector is called a ‘surplus’ balance; a negative balance is called a ‘deficit’ balance. There is nothing inherently bad about deficits, or inherently good about surpluses. If one sector has a surplus balance for a given time period (eg a year), at least one other sector must have a deficit balance. (The only way to avoid deficits is for each individual sector to have a zero balance.)

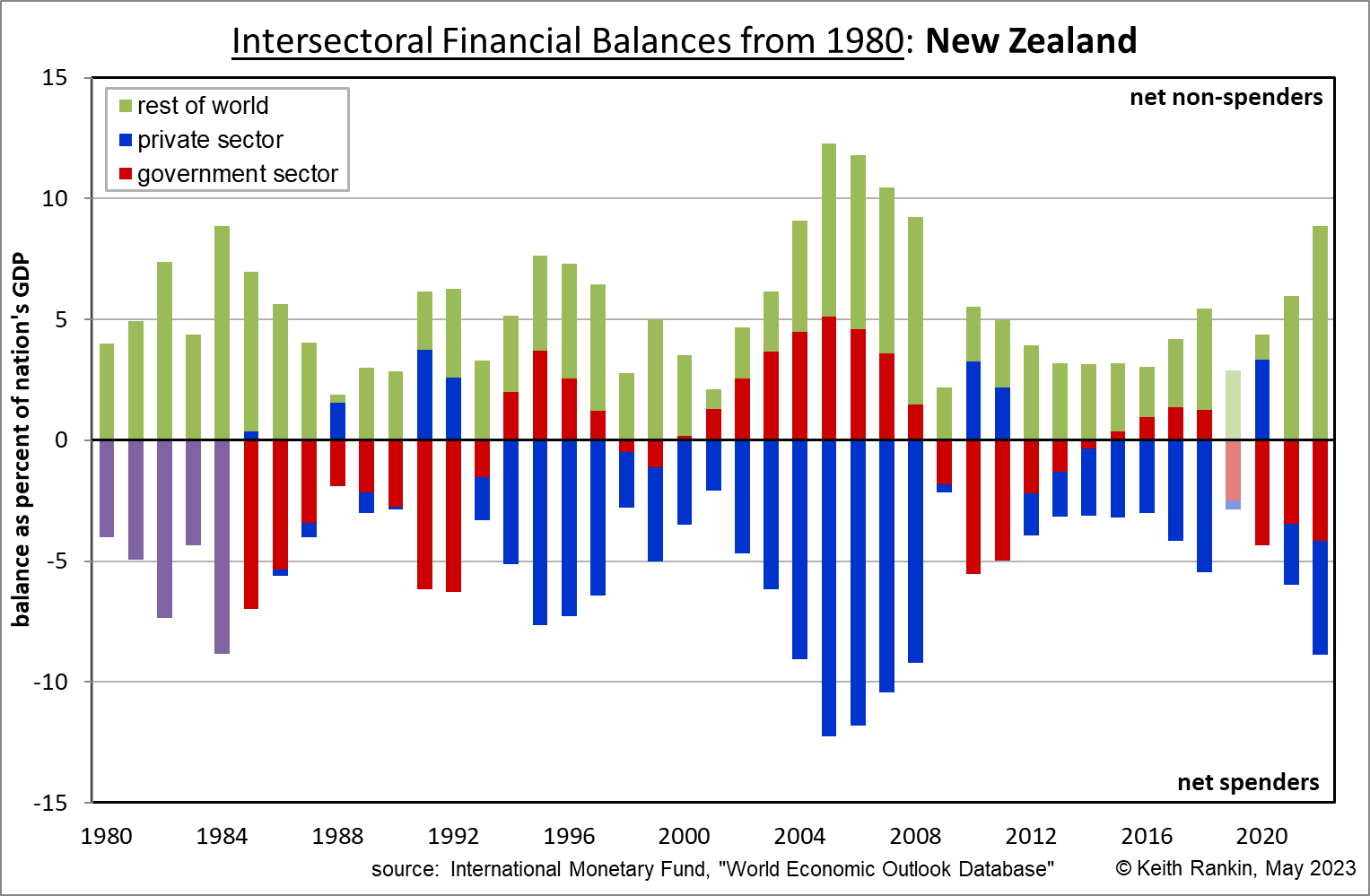

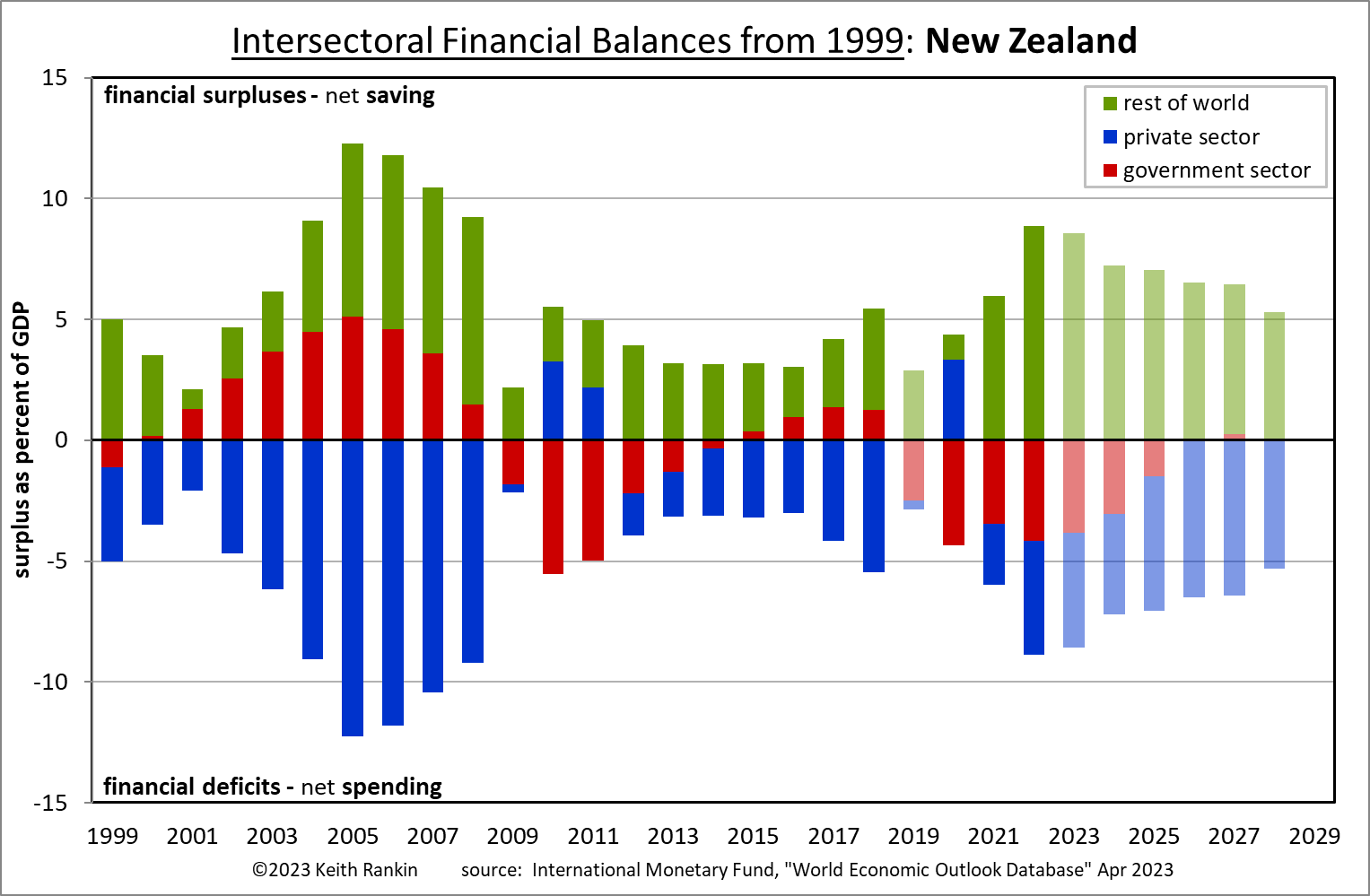

These two charts show Aotearoa New Zealand’s annual financial balances for the three sectors. The first chart goes back to 1980 to show over a longer period whether there is a signature, a recurring annual ‘fingerprint’. The second chart starts at 1999, and includes IMF (International Monetary Fund) forecasts up to 2028. These forecasts are built from a mix of simple projection (‘extrapolation’) from the immediate past and from the country’s financial personality. These charts reveal New Zealand’s political culture with respect to its financial governance.

In these kinds of intersectoral charts, a positive red balance represents a ‘Government sector surplus’ (including local government); a positive blue balance represents a ‘Private sector’ surplus; and a positive green balance represents a ‘Foreign sector surplus’. (Those who’ve studied economics or finance or public policy will understand that a foreign surplus is known in the national accounts as a ‘Current Account deficit’; and that a country with a current account deficit most likely has a trade deficit. So, for shorthand, we may think of a positive green balance as a trade deficit; a situation where imports exceed exports, and where foreign ‘investors’ advance credit to that country.)

A country with repeated foreign-sector surpluses and private-sector deficits may be called a ‘debtor economy’. A country with repeated foreign-sector deficits (ie current account surpluses) and private sector surpluses may be called a ‘saver economy’ or a ‘creditor economy’. We note that NZ Inc is very much a debtor economy. And we note that, for the whole world, there is no foreign sector; so foreign-sector deficits in some countries must be balanced by foreign-sector surpluses in other countries.

New Zealand

If we focus on the second abovementioned chart, there are 24 years of data (1999 to 2022), and six years of forecasts. (We should note that New Zealand and some other southern hemisphere countries have reporting years from July to the following June. So, to get a January to December year, the IMF averages two such July to June years. The result is that the 2019 balances for New Zealand are contaminated by data from the first few months of the 2020 Covid19 pandemic. In reality, 2019 for New Zealand was much like 2018, and I count 2019 as a repeat of 2018.)

For 14 of those 24 years – 2000 to 2008, and 2015 to 2019 – New Zealand has both Government-sector and Foreign-sector surpluses, balanced by Private-sector deficits which are quite big in some years. Further, the pattern of the 2023 to 2028 forecasts reflects the widely understood intent of the New Zealand Government to ‘get back into surplus’. In New Zealand, Government-sector surpluses are seen as a virtue, a statistic that New Zealand governments use to elicit foreign applause.

Other Countries

Examples of other countries’ financial-balance charts can be found in my:

- New Zealand’s Financial Exceptionalism, 31 Aug 2023, Evening Report

- Visualising Countries’ Deficits and Debts, Surpluses and Credits, 29 May 2023, Evening Report

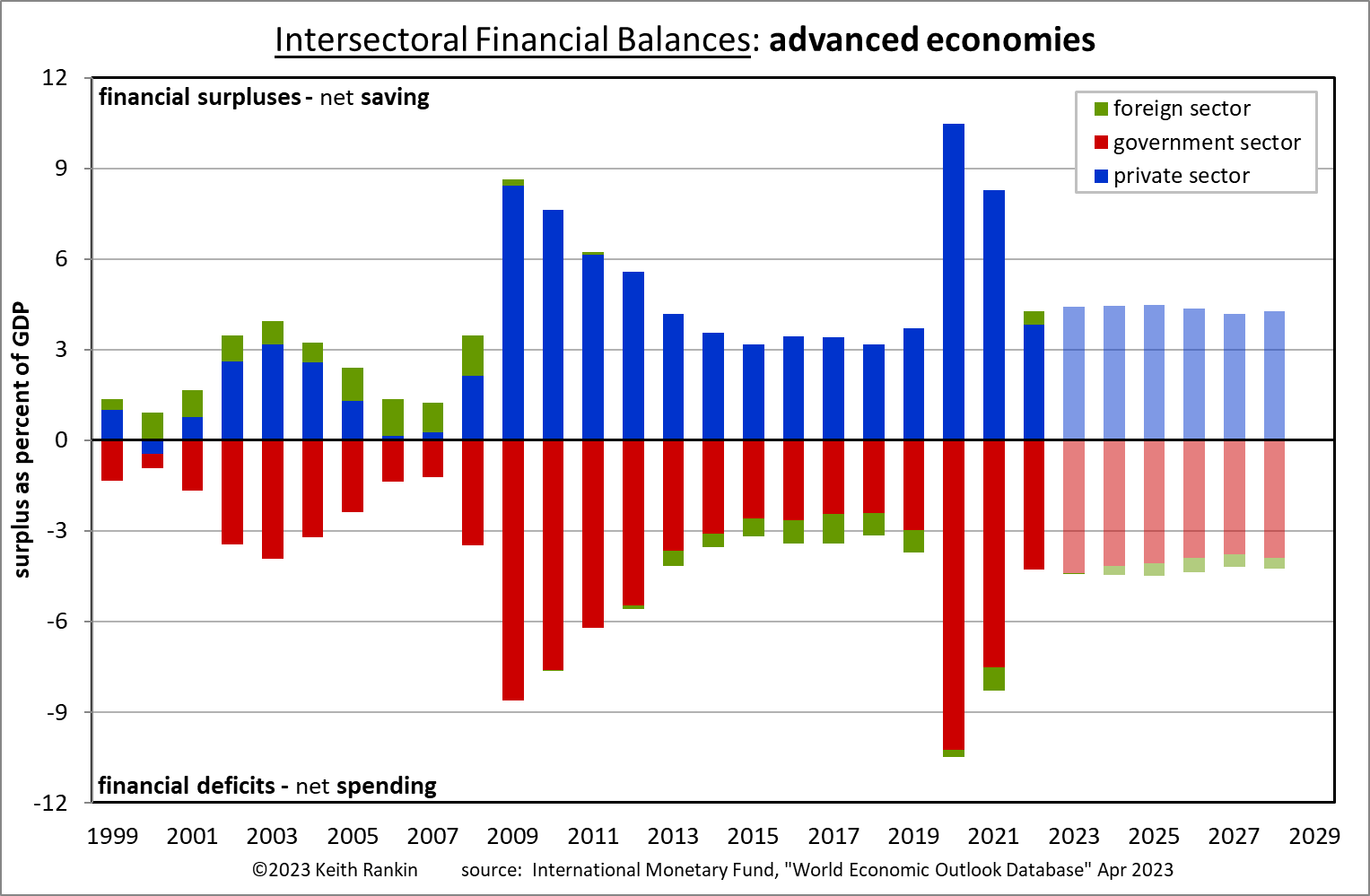

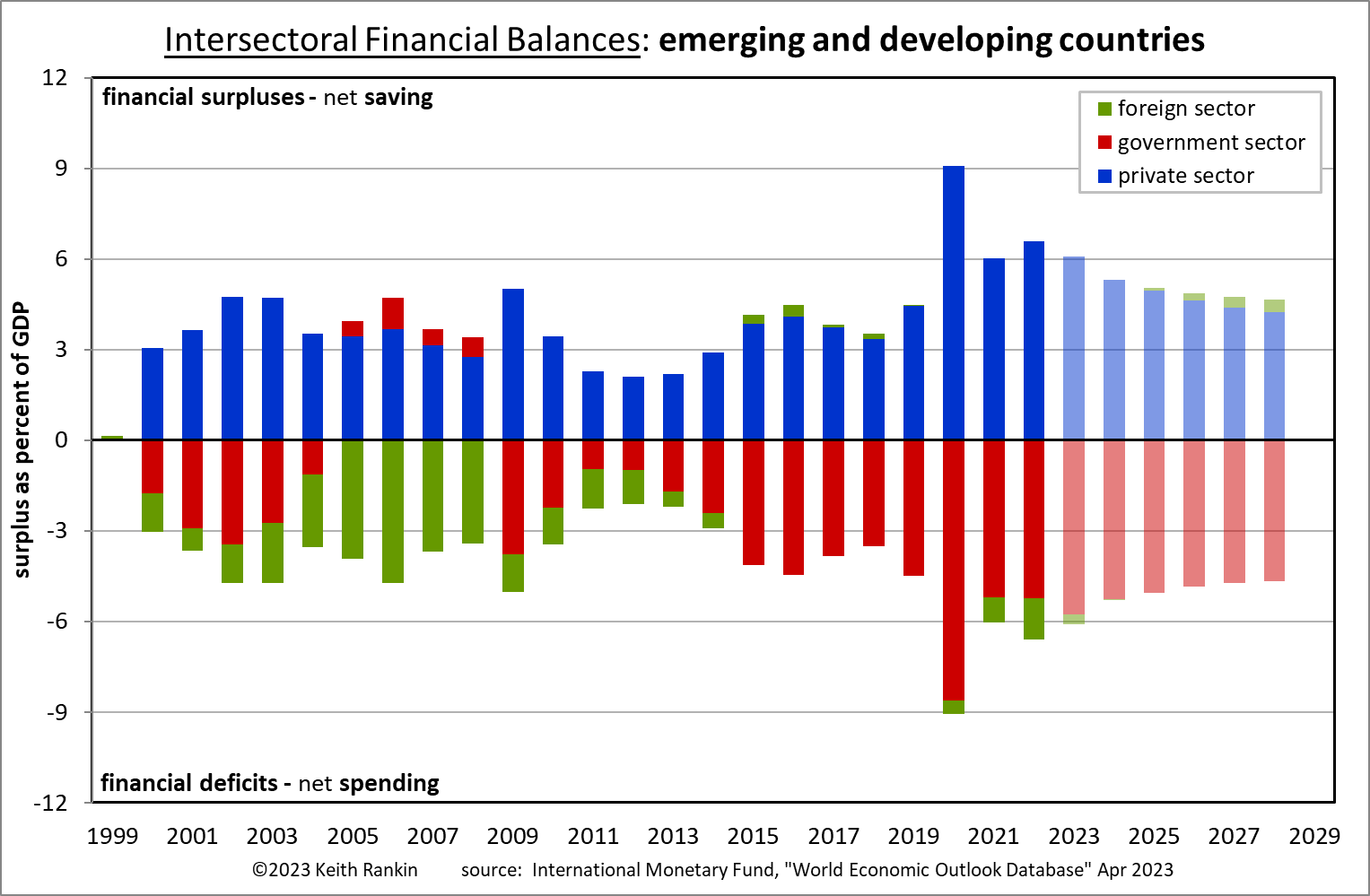

The first-listed of these analyses includes charts for all ‘advanced’ economies combined, and all ’emerging and developing’ economies combined; together those two charts make up the global economy. They show the globally prevalent pattern: private surpluses with government deficits.

Looking at these charts, we see that other countries’ charts look very different from the New Zealand chart. Only Australia has some similarities, and those similarities are diminishing. Australia, becoming more like the norm, has not had a surplus in the Government-sector since 2007.

The one pattern that is particularly rare in other countries is the pattern most common in New Zealand; namely Government and Foreign surpluses with Private deficits.

In my database of financial balances, I have charts for 120 countries. Only three countries have this pattern in the majority of years this century: Tonga, New Zealand, and Lebanon. A clear majority of countries have zero years with this pattern of balances. In other countries, the New Zealand pattern tends to occur ahead of financial crises.

Here is a list of the 40 countries which have two or more instances of the predominant New Zealand profile:

- Tonga: 17 out of 23 years, 2020 most recent

- New Zealand: 14 out of 24 years, 2019 most recent

- Lebanon: 14 out of 22 years, 2017 most recent

- Australia: 8 out of 24 years, 2007 most recent

- Cyprus: 7 out of 24 years (plus forecast years), 2022 most recent

- Estonia: 7 out of 24 years, 2007 most recent

- Turkmenistan: 7 out of 24 years, 2014 most recent

- Kazakhstan: 6 out of 20 years, 2018 most recent, rest before 2008

- Cameroon: 6 out of 23 years, 2008 most recent

- Iceland: 6 out of 23 years, 2007 most recent

- Ireland: 5 out of 23 years, 2019 most recent, rest before 2008

- Bulgaria: 5 out of 23 years, 2004 to 2008

- Democratic Republic of Congo: 5 out of 23 years, 2017 most recent

- Peru: 5 out of 22 years, 2013 most recent

- Cambodia: 4 out of 23 years, 2019 most recent

- Mongolia: 4 out of 24 years, 2022 most recent

- Sudan: 4 out of 24 years, 2010 most recent

- Papua NG: 4 out of 23 years, 2011 most recent

- Rwanda: 4 out of 23 years, 2009 most recent

- Greece: 4 out of 23 years, 2016 to 2019

- Chile: 4 out of 24 years, 2022 most recent

- Jamaica: 4 out of 20 years (plus forecast years), 2019 most recent

- Liberia: 4 out of 22 years, 2013 most recent

- North Macedonia: 4 out of 23 years, 2007 most recent

- Azerbaijan: 4 out of 23 years, 2001 to 2004

- Ecuador: 3 out of 23 years, 2004 most recent

- Paraguay: 3 out of 24 years, 2005 most recent

- Spain: 3 out of 24 years, 2007 most recent

- Samoa: 3 out of 23 years, 2007 most recent

- Fiji: 3 out of 23 years, 2008 most recent

- Panama: 3 out of 23 years, 2008 most recent

- Senegal: 3 out of 23 years, 2004 most recent

- Serbia: 3 out of 22 years, 2018 most recent

- Belarus: 3 out of 22 years, 2019 most recent

- United Kingdom: 3 out of 24 years, 2001 most recent

- United States: 2 out of 24 years, 2000 most recent

- Canada: 2 out of 24 years, 2018 most recent

- Kenya: 2 out of 24 years, 2004 most recent

- South Africa: 2 out of 22 years, 2007 most recent

- Thailand: 2 out of 24 years, 2013 most recent

A key point is that these countries, 40 out of 120 countries, are for the most part (especially the top ten of these) not those which New Zealand readily compares itself with.

A common thread with these countries is that these had this unusual alignment of balances in the years before a financial crisis. This is true for Australia, Estonia, Kazakhstan, Iceland, Ireland, Bulgaria, North Macedonia, Spain, Fiji, Samoa, Panama, UK, USA, South Africa. Countries on to note are Lebanon (formerly known as the ‘Switzerland of the Middle East) which has suffered the worst economic collapse of any country this century); Cyprus, Ireland, Kazakhstan and Panama (which had reputations as tax havens or for money laundering; Cyprus specialising in processing Russian oligarch ‘wealth’); Iceland whose banks ran an overt global Ponzi scheme in the lead-up to the Global Financial Crisis; Greece whose New Zealand style financial signature in 2015 to 2018 was a result of a bail-out settlement, with harsh conditions attached, overseen by the European Commission); and the United Kingdom and United States which had unusual financial conditions during the ‘dotcom’ bubble at the turn of the millennium.

Canada, with a history of stable and unusually low financial imbalances, shows some signs of becoming like New Zealand this decade. Australia on the other hand appears to be maturing, now looking less like Aotearoa New Zealand, and more like other mature capitalist economies.

Turkmenistan is arguably the world’s shyest country, the most hermetic Hermit Kingdom of them all. (North Korea is gregarious in comparison!)

What is New Zealand doing? Monetary and Fiscal policy.

Ostensibly, New Zealand experiences unusually high levels of policy austerity from both the Reserve Bank and from the Treasury ministry. Yet, in a bizarre way, two lots of austerity add up to a privately spendthrift economy; or at least a spendthrift economy in which the new and old social elites consume conspicuously and take advantage of their market power to profit from labour (increasingly an immigrant sub-sector) and beneficiaries.

It’s important to note that, at least for countries well thought of by the international finance houses – and New Zealand is certainly one of those – a certain kind of monetary policy bias is sufficient to bring about the New Zealand’s exceptional financial profile. New Zealand is a popular destination for other countries’ savings.

In summary, professed monetary austerity means that New Zealand has a policy bias towards high interest rates, whose main practical purpose is to keep the $NZ (NZD) exchange rate higher than it would otherwise be; and whose secondary historical purpose has been to appreciate the exchange rate as a way of keeping annual inflation – at least inflation as measured by the CPI (consumers price index) – close to its government-set target. The result is that monetary policy in New Zealand works towards foreign money much as a magnet works towards iron-sand. Comparatively high interest rates keep New Zealand well-lubricated with foreign money; and, in an international crisis, stem the flight of foreign money already here.

(We may note that Sweden and Denmark exhibit the opposite form of financial policy exceptionalism. They have displayed biases towards comparatively low interest rates, an undervalued rather than an overvalued currency, and a strong tendency to ‘invest’ their trade-surplus savings in other countries.)

Secondly, the government’s ‘fiscal austerity’ – it’s “getting back to surplus” bookkeeping policy – means that the government tries to cede all of that incoming foreign money to private sector largesse. Thus, New Zealand’s typical financial situation is that of pools of foreign money being spent by private elites; rampant consumerism amidst resolute government austerity.

Government-sector in dominant capitalist economies

The countries below are the powerhouses of the capitalist world. Unlike New Zealand, they exhibit a mature public debt profile; none are having any problems servicing (ie rolling-over) their government-sector debts. The most vigorous capitalist economies have high levels of public debt. Yet the New Zealand Labour Government has an obsession with getting Government-sector debt down to levels well below first-world norms.

Government-sector debt of leading capitalist economies:

- Japan: 264% of GDP

- Singapore: 168% of GDP

- United States: 129% of GDP

- Canada: 113% of GDP

- United Kingdom: 101% of GDP

- Euro countries: 91% of GDP

- India: 89% of GDP

- China: 77% of GDP

- Brazil: 73% of GDP

- Israel: 61% of GDP

- South Korea: 50% of GDP

- Switzerland: 41% of GDP

- Indonesia: 41% of GDP

Japan’s record high debt has increased little relative to GDP despite running large Government sector deficits every year since the Global Financial crisis. Indeed, a country (such as Japan) with two percent economic growth and three percent inflation can run a five percent annual Government deficit and keep its Government debt at an unchanged level (relative to GDP).

The United States is in a special situation as the world’s money factory. Government debt has become politicised within the United States; nevertheless it is the United States’ Treasury debt that ensures the world economy always has enough money to function.

There are always problems around the distribution of money, of course. The biggest of those problems is that some governments – with New Zealand’s being a prime example – choose to not have enough money. Money has always come to governments via both taxation and debt. That’s how mature capitalism works; government funds its outlays through a mix of revenue and debt. With the exception of a few countries gaining temporary windfall revenues (for example, the oil-rich in recent history), governments should be budgeting for deficits each year. Governments should always be in the red; a simple orthodox guideline would be that (over the economic cycle) annual Government-sector debt averages out at the average economic growth rate plus the average inflation rate. Fortunately, most governments do that (though not necessarily intentionally), maintaining high and stable debt levels.

The New Zealand government does not do this. The result is an elite-only consumer society, with austerity for those not in a privileged situation; certainly not for those who administer austerity. This problem of insufficient government spending is compounded by the way the Government-sector spends the money which it does spend, and noting that elite private sector largesse does yield much tax revenue.

Privileged Employment

Looking at Statistics New Zealand’s Household Labour Force Survey, New Zealand’s elites are employed (or self-employed) in these four burgeoning and privileged employment sectors:

- Professional, scientific, technical, administrative, and support services (up in two years by 18% from 329,000 to 387,000)

- Public administration and safety (up in two years by 25%, from 162,000 to 203,000)

- Financial and insurance services (up in two years by 18%, from 85,000 to 100,000)

- Electricity, gas, water, and waste services (up in two years by 53%, from 24,000 to 37,000)

Much of the money going into these sectors comes directly or indirectly from government spending. On the other hand, these two mainly-government-funded employment sectors are experiencing employment declines:

- Education and training (down in two years by 4%, from 224,000 to 215,000)

- Health care and social assistance (down in two years by over 1%, from 297,000 to 293,000)

Even in these sectors, however, employment of elite managers and the like has grown while employment of teachers and clinicians has fallen. Average managerial salaries in these two service sectors are well above overall average salaries in these sectors.

New Zealand’s exceptionalism is one of increasing elite largesse, and working class and underclass impoverishment. New Zealand has burgeoning elites – now perhaps 20% of the population – who benefit from the exceptional combination of monetary and fiscal austerity. However, as Peter Turchin (author of End Times, 2023) predicts, in coming economic and financial crises there likely will be increased competition between sub-elites as the top echelons go through a process of becoming smaller and even more elite. (See New science explains the rise of political instability, oligarchy and elites, by Danyl McLaughlan, NZ Listener, 22 August 2023.)

The elites are both of the political ‘right’ and the political ‘left’. Politics becomes a game between these two tribal sub-elites.

In Short

While, so far, this process of ‘elitification’ – the entrenching privilege of the top 20 percent in economically advanced countries – is far from unique to Aotearoa New Zealand, this country’s exceptional financial policymaking certainly is very much a part of the domestic problem. New Zealand’s twenty-percenters live as if New Zealand was a much more prosperous country than it actually is. And, thanks to governments’ love of financial surpluses above other measures of administrative success, private elite prosperity does not filter down to the increasingly indebted 80 percent.

————-

Keith Rankin (keith at rankin dot nz), trained as an economic historian, is a retired lecturer in Economics and Statistics. He lives in Auckland, New Zealand.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}