I have written elsewhere (see reference list below) about the important principles that suggest all enfranchised residents should receive a share of public income, and how the realisation of this is essentially a matter of reformed public accounting.

Here I just consider two typical New Zealanders of different generations, and two policy options. And no jargon.

Policy Options:

-

- Complex option; the status quo.

- Simple option: all New Zealanders over 18 receive a universal dividend of $175 per week; additionally, New Zealanders over 65 get a universal superannuation of $171 per week; all income is taxed at 33 cents in the dollar. (The two universal payments combine to $18,000 per year.)

Example People:

-

- ‘Married’ persons aged over 65.

- ‘Married’ persons with children, aged 18 to 64, with partners grossing around $35,000 a year. At lower household incomes, they qualify for Working for Families ‘tax credits’ and Accommodation Supplements.

Example People Findings

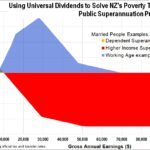

The chart looks at differences in the available weekly incomes of these example people, as their gross annual incomes vary from $0 to $100,000 per year; that is, the differences that would apply if Policy Option 1 was replaced by Policy Option 2.

(Note on Policy Option 1. Working for Families ‘tax credits’ are generally paid to children’s caregiver parents. Typically, the caregivers would be the lower earning parents. However, in the scenario here, Example People 2 may be earning more or less than their partners, depending where they are on the chart’s income scale. To deal with this I have attributed these payments equally to each parent.)

(Note on Policy Option 2. This option regards a ‘superannuitant’ as any New Zealander aged over 65, and ‘beneficiary’ as being any New Zealander aged 18-64 who presently receives total public benefits in excess of $175 per week. With Policy Option 2, the first $175 per week of beneficiaries’ benefits becomes an unconditional universal dividend. The remainder continues to be a conditional payment.)

The chart shows that, for Policy Option 2, Example People 1 (‘senior citizens’) would gain about $30 per week if they have zero private earnings. That weekly gain falls to $0 per week if they gross $10,000 in a tax year. Senior citizens earning around $35,000 would be around $60 worse off under Policy Option 2 than under Policy Option 1. Higher earning seniors would be $70 per week worse off. The main losers from Option 2 would be higher earning superannuitants.

The blue part of the chart shows that no working age people would be worse off than at present, and that some would gain. Their actual gains arising from Policy Option 2, which would vary from person to person, peak in our case at around $28,000. The main gainers from Option 2 would be minimum wage workers, and many part-time workers whose earnings are critical to their household budgets.

It is important to note that people of working age earning over $70,000 per year would experience no change. And persons earning between $50,000 and $70,000 – nearly half of all fulltime workers, would gain up to $10 per week.

Other Benefits of Policy Option 2

An important group of gainers would be young people – for example 20 24 year olds – a number of whom are dependent on their parents; others are beneficiaries trapped in benefit poverty. One of the great misfortunes of our times is the difficulty too many young people face in making the transition to economic independence, and to the personal autonomy that ensues from economic independence.

If we consider beneficiaries in general, this policy will not give them any more money directly. But, by allowing them to keep their universal dividend when they take on more paid work, the policy removes their poverty traps.

Policy Option 2 ticks all the boxes: it is affordable, it is simple, it is democratic, and it effectively redistributes income from comfortably off ‘boomers’ to ‘Gen-X’ ‘battlers’ and to millennials struggling in an environment of punitive benefits and precarious work. Option 2 also facilitates fulltime workers (eg 40 hour per week workers) to work fewer hours (eg 30 hours per week) and to live less stressed lives. It is a ‘win win win win win’ policy option. That’s five wins. Further, there would be a reduction in requirement for bureaucratic services as fewer people would seek help through conditional benefits. Tax collection would be substantially simplified.

There are simple and affordable solutions to our seemingly intransigent income distribution problems. It just requires a willingness to see. Thinking that feels bold to one generation, once absorbed, becomes commonsense to the next generation. Traditional ‘National Party’ tax cut policies are blighted by the fact that higher earners gain more than lower earners. In Policy Option 2, the gains go to where they are needed, the rich gain nothing, and the old rich become worse off.

Less targeting of benefits can mean better targeting. Less can be more.

Select Publications:

2019: http://socialalternatives.com/issues/basic-income-and-new-universalism

2018: https://www.nzae.org.nz/events/nzae-conference-2018/2018-conference-papers

2017: https://thepolicyobservatory.aut.ac.nz/publications/public-equity-and-tax-benefit-reform

2016: https://scholarworks.wmich.edu/jssw/vol43/iss3/5/

2011: https://www.nzae.org.nz/events/nzae-conference-2011/programme