Analysis by Keith Rankin.

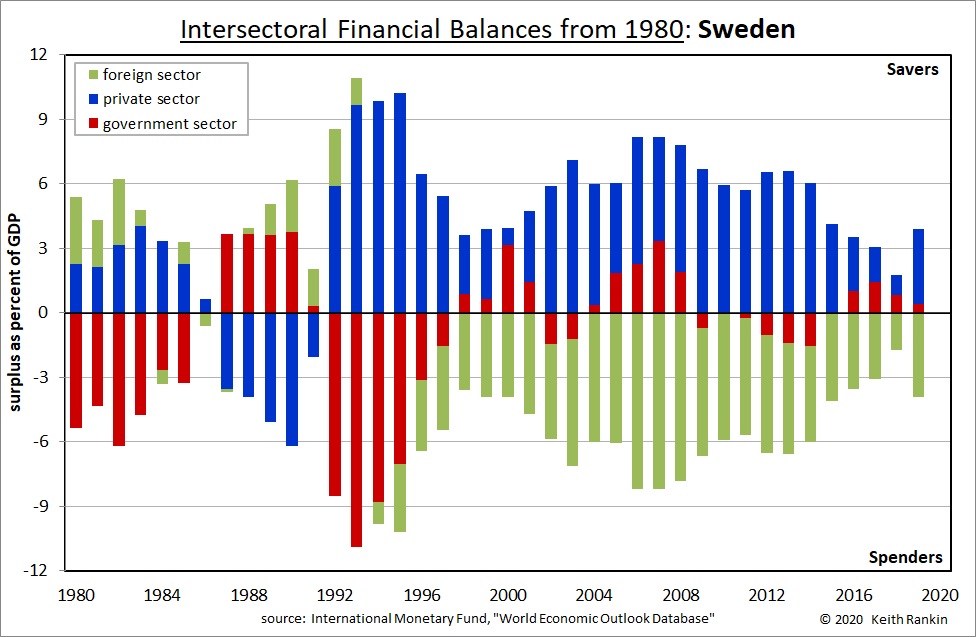

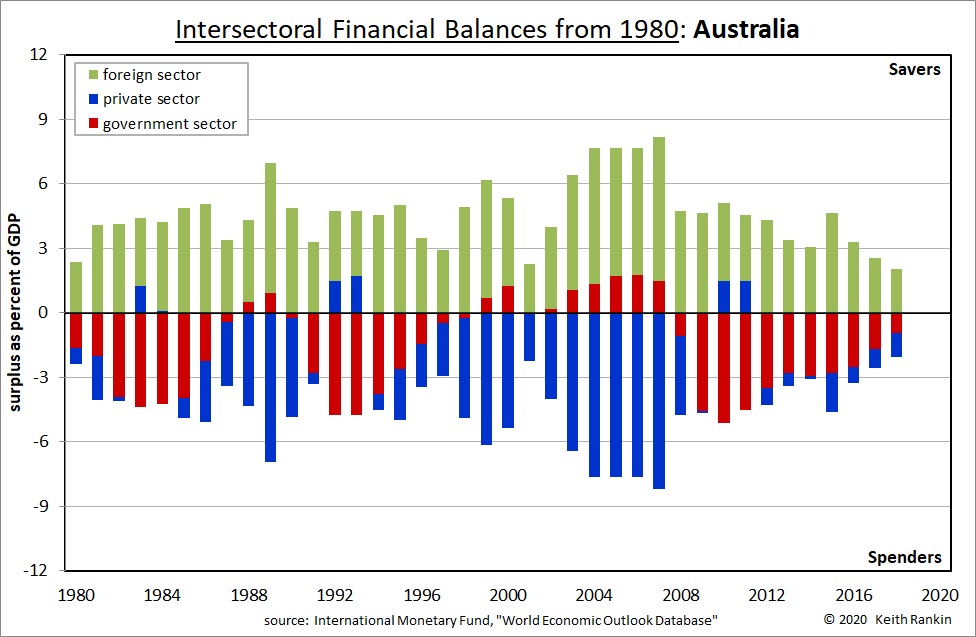

1980s: Sweden like New Zealand and Australia

Sweden in the 1980s, financially speaking, looked something like New Zealand and Australia. It was a period of stress from high oil prices, and global inflation. Governments ‘took up the slack’, running deficit balances. In Sweden, the slack was caused mainly by private-sector surpluses. In Australia it was due to an absence of private-sector deficits. So, in both countries, ‘the slack’ was due to less-than-normal private sector spending.

All three countries drew on foreign savings in the early 1980s, as shown by the green foreign-sector surpluses. This largely reflected high oil prices; the main creditor countries were then oil-exporting countries.

The above charts compare and contrast the financial experiences of Sweden and Australia. (Note that, for technical reasons, Australia’s chart only goes to 2018. The problem is that the Australian figure for 2019 is an estimate that makes use of government budget forecasts to June 2020. Thus, the IMF statistic for 2019 is distorted by the impact of the coronavirus pandemic in 2020.)

Changes took place in the mid-1980s, as financial markets freed up in the wake of neoliberal reforms, and as oil price falls in 1986 entrenched an optimistic mood in financial markets. New Zealand led the liberalising way in 1985, followed by Sweden in 1986, and Australia towards the end of 1986. This is shown for Sweden and Australia by the switch to substantial private sector deficits; these private deficits then enabled their governments to run budget surpluses in the late 1980s. These private deficits involved much speculation in financial and real estate assets. High interest rates at the time discouraged normal business borrowing.

At this point New Zealand was different, having its financial crisis in 1987. Sweden and Australia had their financial crashes in 1991. While in Sweden it was worse than Australia, both countries had banking crises; banks failed.

Sweden in the 1990s: from one panic to another

In the early 1990s, in both Sweden and Australia, government budget deficits ran high, as governments accommodated private sector surpluses by running balancing deficits. Australia took a relaxed approach through the decade, continuing its historically normal willingness to borrow from overseas, running government budget deficits consistent with its historical practice (though quite different from the late 1980s).

The financial panic spooked Sweden’s policymakers. The government had to run very large deficits in the early 1990s, in response to the greater level of insolvency and panic in Sweden’s private sector. Further, this new government debt added to debt from in the early 1980s’ deficits (and presumably the late 1970s, though the IMF data source does not go back that far).

Sweden went on to a policy to repay debt. From 1994, Sweden started to repay its external debt, as shown by the ‘green’ foreign sector balance moving into deficit. This meant that Swedes were now earning more than they were spending (exporting more than they were importing), a situation that they were more culturally comfortable with than the situation they were in, in the 1980s.

From 1996 the Swedish government moved to a strong public austerity policy, to repay its public debt. In doing so, they were disadvantaging the career prospects of the generation born in the early 1970s. When there is a government-sector austerity programme in place, it is always the generation born around 25 years earlier who suffer.

The Swedish economy went into a second contraction in 1996, with unemployment in 1997 exceeding its highs from the financial crisis at the beginning of that decade.

The Swedes adopted an ongoing mercantilist policy of export-led growth. By 1998, both Sweden’s government and private sectors were running surplus balances, with the unspent surplus income being invested outside of Sweden; indeed spent in countries like Australia which continued to spend surplus incomes generated in countries like Sweden which were reticent to spend.

Twenty-first Century Sweden: classic mercantilist signature

Sweden’s economic pattern looks very stable this century; persistent private sector surpluses and foreign sector deficits. Further, unemployment stabilised between six and eight percent, albeit in a country which represents the epitome of the protestant work ethic. At the same time, Australia’s unemployment stabilised in the four to six percent range.

In the period from 1980 to 1992, Sweden’s and Australia’s charts look similar (though Sweden’s balances were more accentuated). From the mid-1990s, however, their charts look opposite, though both being dominated by the private and foreign sectors. Sweden adopted a mercantilist strategy, while Australia happily accepted an anti-mercantilist signature. This is not to say that Australia doesn’t care about exports; it’s just that Australia spends its export earnings (and more), while Sweden wants others to spend Sweden’s export earnings.

This want of Sweden is able to be satisfied, because not all countries share that ‘want’. The signatures of Sweden and Australia, this century, are complementary to each other.

Neither country has anything that could be regarded as a debt problem – neither external debt nor government debt. Sweden, this century, is very much a creditor economy, while Australia is a debtor economy. It just means that Australia spends more than it earns and Sweden spends less than it earns. Both countries’ peoples seem happy with that arrangement.

Re government debt, we see that Australia has been relaxed about running budget deficits in the 2010s; more so than New Zealand and far more so than Sweden.

Sweden’s undervalued exchange rate

Sweden runs its mercantilist economy by having an undervalued currency (Swedish krona); to do this Sweden has had to have negative wholesale interest rates from 2015.

Sweden has been running large trade surpluses (exports exceeding imports; shown in the chart as foreign sector deficits) since the mid-1990s. So have the northern Eurozone countries, since 2000. In the 2000s the northern Eurozone countries ran their trade surpluses within the Eurozone. Since 2010 they have been competing with Sweden to run trade surpluses with the non-European world. These northern Eurozone countries use the Euro as a means to have an undervalued currency; this mean that – had they retained the Deutschmark, Guilder and Shilling – those currencies would have been trading at higher rates against the US dollar.

This Euro effect – which gives Germany an undervalued currency – has been a godsend to countries like Germany and Netherlands, with their mercantilist economic cultures. But it has placed pressure on the other northern European countries – also with mercantilist economic cultures – which are not in the Eurozone: Sweden, Denmark, and Switzerland. Thus, it is no coincidence that these are the countries which have had negative interest rates since around 2014. (Norway has not needed negative interest rates; it has been an oil exporter.) They do this to stop their exchange rate appreciating against the Euro.

To Finish

Sweden reverted to its cultural type this century – a type that extends back at least to Viking times – as a country that feels most comfortable when accumulating treasure; that is, gaining foreign credits which could be spent on imports, but probably never will be. (The Vikings hoarded much of their ill-gotten treasure.) Further, Sweden has gone to the extent of having negative interest rates for five consecutive years, as a way of ensuring its ongoing export ‘competitiveness’.

If too many other countries behave in the same way as Sweden, we could see an ‘interesting’ (in the Chinese sense of ‘interesting times’) ‘race to the [global] bottom’. The biggest danger here is that the United States – under overtly mercantilist leadership from 2017 – will make a serious attempt to abstain from its cultural type, and try to run financial balances akin to those of Sweden and Germany.

Fortunately, these overtly mercantilist tendencies are countered by the much more relaxed financial strategies of countries like Australia. The most important feature of Australia’s chart is the willingness of the Australian private and government sectors to run deficit balances.

{kind=link}