Chart Analysis by Keith Rankin.

Most countries’ economies have financial signatures that reflect their cultures and histories. We may, in a binary sense, call these surplus and deficit signatures. But there are a number of important nuances.

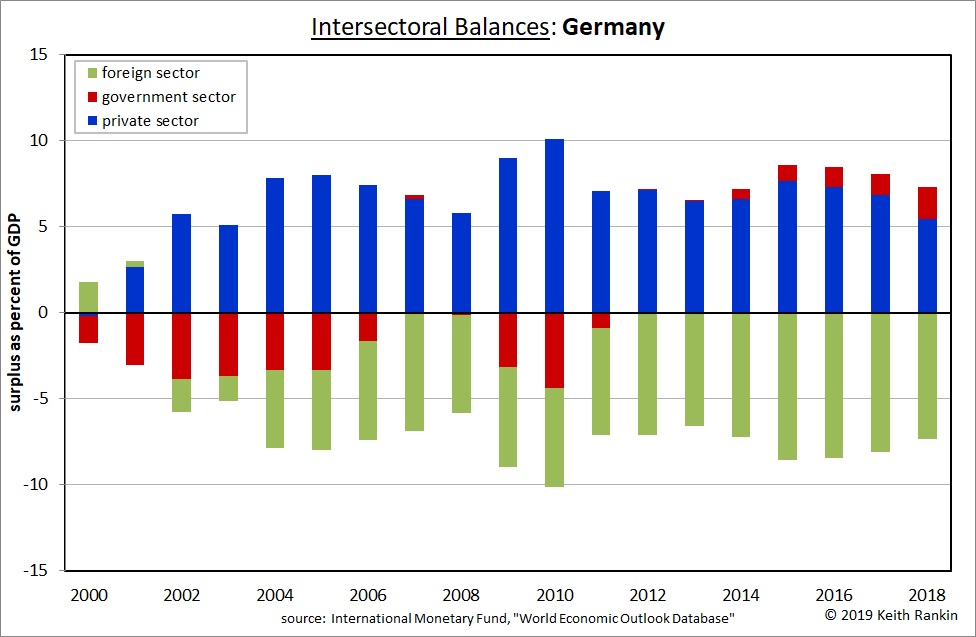

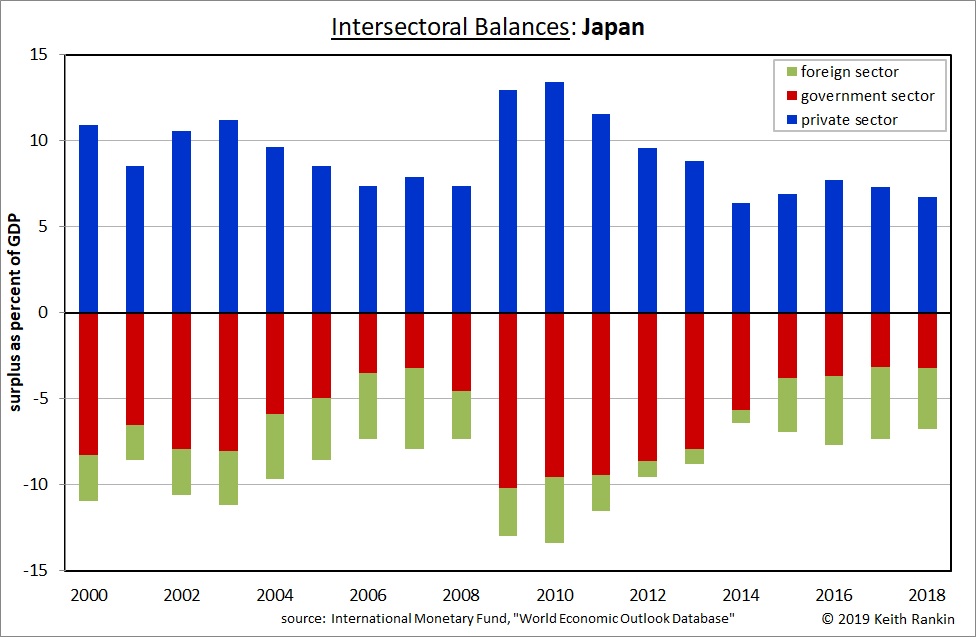

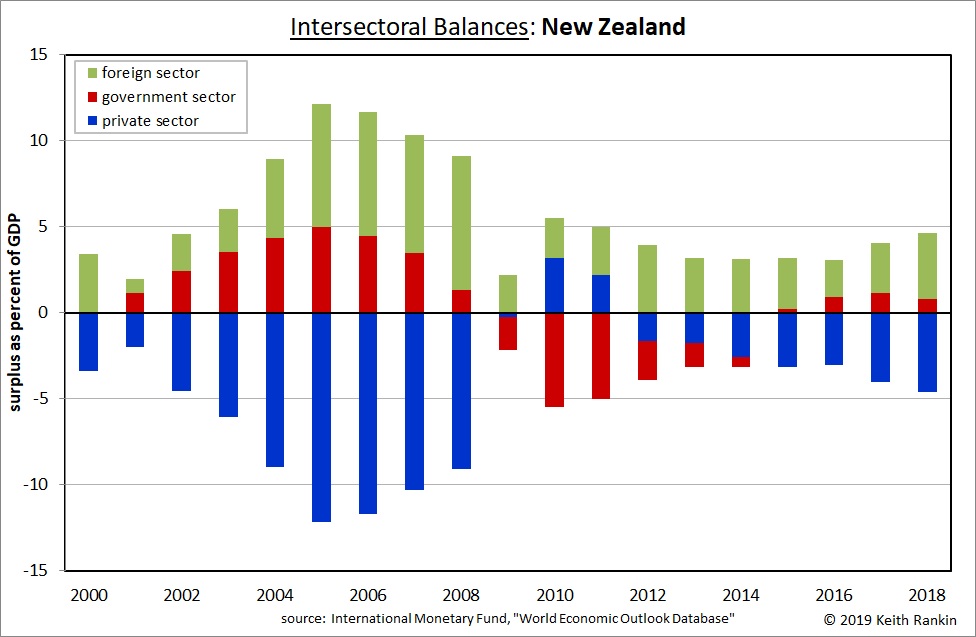

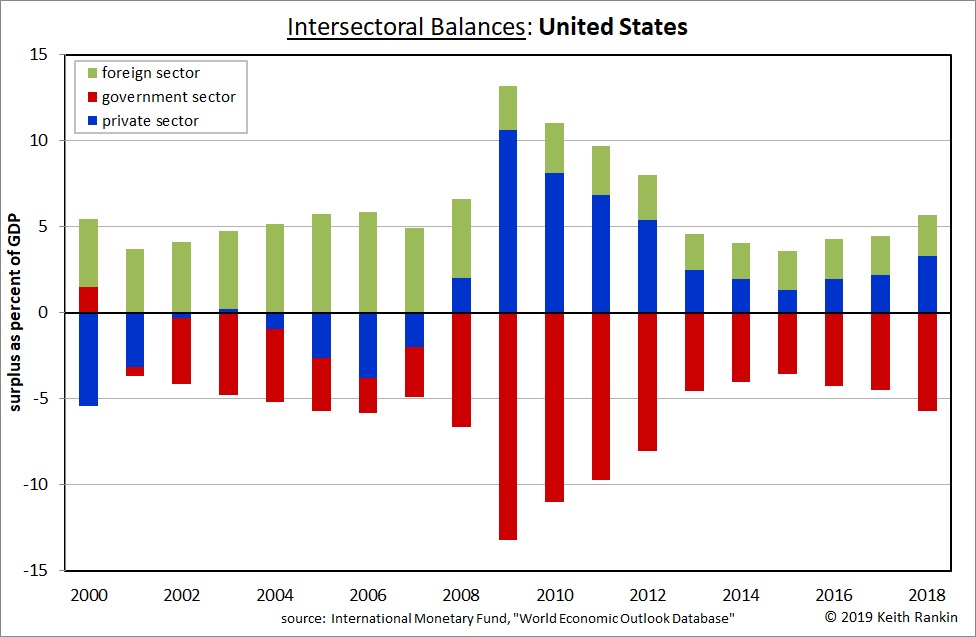

For these four developed countries, Germany and Japan would be classed as having ‘surplus’ economies, while New Zealand and the United States would be classed as ‘deficit’ economies. The key to this classification is the green-shaded ‘foreign balance’.

Germany and Japan consistently show substantial negative foreign balances, meaning that their resident households, businesses and governments spend less than their national income, requiring other countries’ economies to purchase their unbought goods and services. This pattern is most clear for Germany, where, for every year since 2004, more than five percent of Germany’s available output has been enjoyed outside of Germany. It means that, in this era of low inflation, the German economy is accumulating substantial financial credits with respect to the rest of the world.

The problem for Germany is that, in order to spend those credits, it would have to become a deficit country. And that would not sit easy with Germany’s financial culture. Germany is a classic ‘mercantilist’ nation, as are a number of other northern European countries. The historical consequence of a country not using its credits is to lose them. Thus, in historical time, Germany’s negative foreign balances can be understood as an ongoing beneficial subsidy (ie gift) to the rest of the world.

The dominant signature feature that is shared by Germany and Japan is the persistence of large private‑sector surplus (net positive) balances. These are cultural signatures, not temporary features that vary substantially in historical time. They represent the savings’ cultures of the citizenry of these countries.

However, in Japan (unlike Germany, which subsidises its foreign sector), the main beneficiary is Japan’s government(s). Japanese citizens are more resistant to taxation than are German citizens. Rather than pay more taxes, they like to lend to their government, albeit at close to zero percent interest. Private income that Germans give up in taxes is, in Japan, held by Japanese citizens as government loans. The Japan option serves as a form of citizens’ insurance. By accounting for much more government spending as debt in Japan than in Germany, individual Japanese citizens experiencing ‘rainy days’ can effectively reclaim income that had been made available to their government.

While clearly very successful and effective, Japan’s financial policies are commonly dismissed in the west as ‘unsound’ Modern Monetary Theory.

New Zealand is a clear counterpart of Germany, a historical beneficiary of the kinds of subsidies that Germany and similar countries confer on their foreign sectors. New Zealand is unusual in that its cultural signature is one of private (business and household) financial deficits, funded by unspent income in countries like Germany. This pattern is quite financially sustainable. If New Zealand averages three percent economic growth and two percent inflation (these are our policy targets) then a foreign sector subsidy (also called ‘current account deficit’) of five percent of GDP each year will not add to the indebtedness burden of New Zealanders. In recent years that annual inflow has been averaging about three percent of GDP.

Like New Zealand, the United States is a beneficiary in the global financial order. While this is cultural – the pattern shows in all Anglo countries – it is also a consequence of the role of the US dollar as the world’s reserve currency.

Unlike New Zealand, the United States has a signature pattern of private sector surpluses. And, like Japan, the United States has a strong pattern of government deficits. The result is that American governments (especially the federal government) is the most significant net beneficiary of both German‑style foreign subsidies and (as in Japan) of private domestic savings. The government spends what the private sector does not spend. Indeed, the United States’ signature government deficit represents the single most important balancing act that prevents global financial collapse.