Interest rates, though headline‑rousing when it comes to mortgages, are an arcane and deeply mysterious component of economic life.

The received wisdom is that they represent the ‘time‑value of money’, and therefore should always be positive. Low interest rates are supposed to indicate a high willingness to postpone consumer pleasures. Interest income is also understood as an entitlement, a reward for hoarding rather than spending money.

In macroeconomics, we are told that low interest rates indicate ‘loose money’, which in turn means higher inflation. And we are told that we must engineer interest rates upwards as a means of curbing both residential land prices (‘house prices’ in common parlance) and consumer prices. Recessions are known to be collateral damage of upwardly‑engineered interest rates; but recessions pass, we are also told.

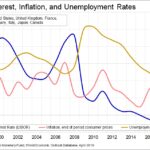

Much of our evidence is from individual nations’ statistics. The problem here is the way countries’ currency exchange rates confuse the picture. By looking here at G7 data, we have the worlds predominant capitalist countries taken together rather than individually. The exchange rate movements between their currencies largely cancel out.

On its own, the charts shows an ambiguous relationship between interest rates and inflation. We should note however, that conventional wisdom suggests it takes around two years for rising interest rates to curb inflation, and for falling interest rates to raise inflation.

The chart shows interest and inflation rates, using the percentage rates on the left‑side axis of the chart. Unemployment rates are read using the right‑side chart axis.

There are certainly instances where falling interest rates are followed by rising inflation – eg early 2000s. And falling interest rates (2009, 2012) followed by rising inflation. We might note that the rising inflation in 2010 and 2011 was mainly due to fiscal stimulus (rather than due to low interest rates); governments choosing to run the very high budget deficits that enabled recovery from the Global Financial Crisis.

In recent years, falling interest rates since 2011 have not been able to raise inflation above the annual two‑percent that is optimal to keep the wheels of capitalism spinning. And interest rates sure have come down. The key global interbank rate – the LIBOR – has been below zero since 2015.

We see that the relationship between interest rates and unemployment is rather more compelling than that between interest and inflation. Rising interest rates clearly bring‑about higher unemployment. Further, it is the rising unemployment that typically – but not always – induces lower inflation. In the chart, falling interest rates were followed by falling unemployment. Unemployment rates, our most critical indicator of recession, show that recessions have been the critical instigator of low inflation.

Indeed, it is fair to say that rising interest rates only curb inflation by creating contractionary conditions; creating recessions or near‑recessions. There is no direct connection between ‘loose money’ (indicated by low interest rates) and ‘high inflation’; or between ‘tight money’ and low inflation’.

By pre-2015 conventions, the developed world liberal‑capitalist economy is now in a sweet spot; low inflation, low unemployment. Annual economic growth is at potentially sustainable levels (eg 2% rather than 3%+). Yet there is much anxiety. Much of the anxiety among the richest 10% is because there were other motives – other than disinflation – for past high interest rate policies. It was through these monetary policies that the 1980 to 2008 ‘class‑war’ between capital and labour was waged. High and compounding interest was understood then as a free lunch by the rich, a means of transferring wealth directly from the poor to the rich.

The 2020s will bring new economic challenges; the challenge of low inflation and negative interest rates as the new norm. This happy state of affairs will not last though, so long as we have economic policy frameworks rooted in the 20th century. Labour shortages are now the big challenge of global capitalism. If policymakers fail to see this – and persevere with fiscal austerity policies (as we see in New Zealand) – then in the late 2020s we should expect a new form of stagflation; high inflation and structural unemployment.