Keith Rankin Analysis: New Zealand’s Cyclical Growth Contractions

In 1939, Joseph Schumpeter published his magnum opus, Business Cycles. He emphasised three growth cycles, Kitchin (about every three years), Juglar (about every decade) and Kondratiev (about five decades). Of interest to us at present is the Juglar Cycle, with its frequency of about 10 years.

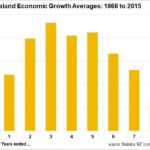

This month’s chart averages economic growth (adjusted for inflation but not population). It suggests a very definite problem around years ending in ‘8’. Most observers of New Zealand’s macroeconomic history would be unsurprised. The ‘8’ years, with a few exceptions, have been characterised in New Zealand by contractionary economic conditions.

Interestingly, the next lowest year is not an adjacent year (‘7’ or ‘9’); rather it’s the ‘1’ year. Indeed, if I was to do this exercise for the world economy as a whole, the ‘1’ year would probably be that with the least growth (notwithstanding the global financial crisis of 2008).

Next year is an ‘8’ year. And all the indications – except one – suggest that 2018 will be a repeat of 2008; in New Zealand and in the world. The exception is that interest rates are much lower than they were in 2007, and the monetary authorities in some countries have their heads around negative interest rates. This in my view means that the world economy should ride out 2018 more easily than it did 2008.

I’m less confident about New Zealand. In the 1930s, countries that had made liberal adjustments (in welfare especially, and in monetary policy) in the 1920s (eg United Kingdom, Sweden) did best. Countries that most practiced fiscal ‘soundness’ in the late 1920s – United States, France, Germany – suffered worst.

My sense is that New Zealand’s lucky run this century is about to unravel. If that unravelling starts next year (or even sooner, if too much real estate is offered for sale after the 2017 election), I am not confident that New Zealand’s public sector will be prepared to go into large-scale deficit spending. I’m particularly worried that a new Labour-led government might pursue debt-averse austerity policies in the event of a 2018 recession.

The last years in which Schumpeter’s three cycles had simultaneous downturns – globally – were 1931 and 1981. While 1931 was particularly bad in New Zealand, 1981 was surprisingly OK in New Zealand compared to the rest of the world.

My sense is that the worst of economic times will happen in the decade from 2025 to 2035. 2028 (or 2027) may be particularly bad in New Zealand, as 1927 was. The next eight or nine years are the ones that will be critical. We need a genuine contest of ideas. We should be prepared for the critical consequences of inequality, precarious living, spending collapses, and debt-deflation.

The world capitalist economy grows through a process of debt-leverage. Every 10 years sees a bout of deleverage; sometimes regional, sometimes global. The solution to deleverage in the past has mainly been to quickly re-establish the leverage cycle. It didn’t happen in the USA, France and Germany in the 1930s. After one of the ‘8’ years or ‘1’ years in the next decade or two, the traditional monetary reboot will not work. We need to have a Plan B that is better than the World War that followed the Great Depression of the 1930s.