Analysis by Keith Rankin.

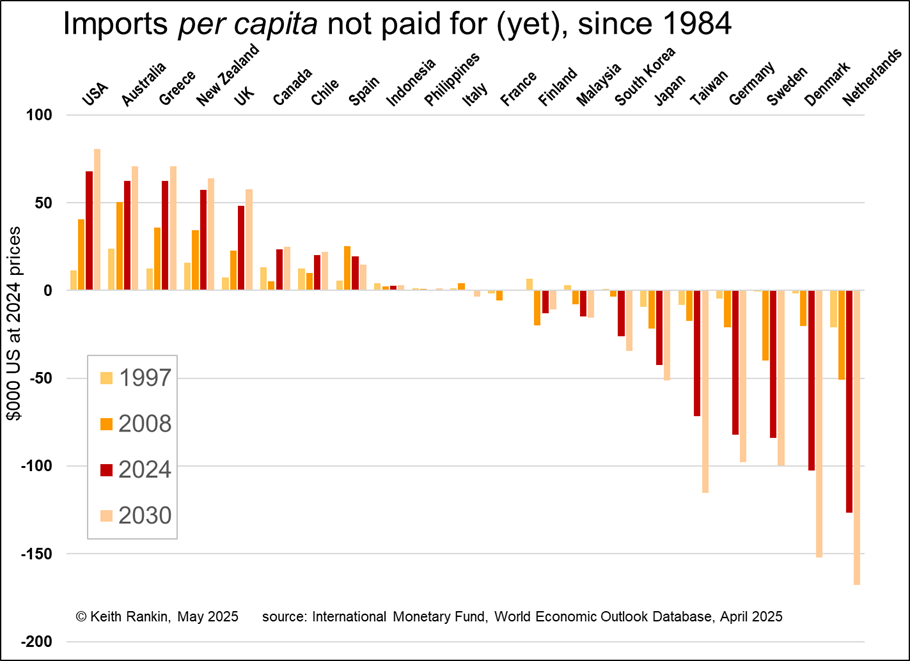

The ‘see-saw’ chart above shows the accumulated ‘excess benefits’ that Aotearoa New Zealand, and a few other countries, have enjoyed from international trade over the last 40 years. These are benefits arising from ‘unbalanced trade’ which are in addition to the regular benefits – arising from efficient specialisation – of ‘balanced’ world trade. Real world trade is a mix of ‘balanced’ (paid for) and ‘unbalanced’ (on forever-credit).

The excess benefit data shown is an inflation-adjusted accumulation of the United States’ current account deficits. We remember that the benefits of trade are what (goods and services) you get, not what you give up.

We note here that the United States is a ‘winner’; not the loser which Donald Trump claims that it has been. The United States has enjoyed $70,000 worth of excess trade benefits over 40 years, per American. And it is projected to enjoy another $10,000 worth of excess trade benefits over the next seven years.

So, what is Donald Trump grumping about? Rhetorically, why does he aspire that ‘America’ should be like Germany?

The biggest losers, as shown here, are a group of northwest European countries, plus Taiwan. (For lack of a complete set of data from 1984, China is not shown here. But China would fit into the chart next to Malaysia. While China has significant accumulated trade surpluses, these are spread over a very large population.) The losers are the countries which have – in effect – ‘given’ away lots of stuff; exports for which they have not received anything in return and will probably never receive anything in return.

The 2030 projections show that these ‘surplus’ countries will continue to under-import; they are not projected to claim the imports that are rightfully theirs to enjoy. Rather, the deficit countries will most likely continue to enjoy these excess unpaid-for benefits.

(There are at least two other ‘surplus countries’ – countries like Germany and Sweden – which would be ‘off the chart’: Singapore and Norway. And one other deficit country: Türkiye.)

Discussion

With international trade in any given year, surplus countries ‘give’ goods and services to deficit countries. They give ‘with strings’. The most obvious form of ‘string’ is a return gift next year; a fully commercial kind of ‘string’ would be a return gift with interest.

For example, if Sweden exports US$1,100 million worth of stuff (ie goods and services) to New Zealand in 2025, and New Zealand exports $1,000 million worth of stuff to Sweden in 2025, then the 2025 gift is $100 million worth of stuff from Sweden to New Zealand. (In technical language, and from New Zealand’s viewpoint this gift from Sweden is called a bilateral trade deficit; from Sweden’s point of view, it’s a trade surplus.)

A return gift with 3% interest would be $103 million worth of stuff from New Zealand to Sweden. (This would be a New Zealand bilateral trade surplus – a deficit for Sweden – in 2026.) The bilateral – ie two-country – ledger would be settled. Effectively, in this example, Sweden lends $100 million of stuff to New Zealand in 2025, and New Zealand repays the loan, with interest, in 2026. Gifts ‘with strings’ are debts.

There are two potential problems. The first problem is that New Zealand may not be able to sufficiently increase, in one year, its exports to Sweden (eg from $1,000 million to $1,203 million, assuming unchanged imports from Sweden). One solution might be for New Zealand to increase its exports by that amount to other countries, and for other countries to export $203 million more to Sweden. But that increase in exports of $203 million might still be too difficult for New Zealand to accomplish in 2026, regardless of who the buyers are. New Zealand might need to borrow more in 2026, (or to import less,) or to repay its 2025 trade debits further into the future.

Indeed, New Zealand might prefer something like a 40-year mortgage. New Zealand could run trade surpluses re Sweden (ie Sweden running deficits) of about 4,358,000 each year for 40 years. In total, over the 40 years from 2026 to 2065, Sweden would receive stuff worth $174,323,300 as its ‘return gift’.

The second (much larger) ‘problem’ is that Sweden might not want to run a trade deficit at all; that is, Sweden might not want to be repaid (except, that is, in some imaginary never-never timeframe). Whether this qualifies as a problem depends on a person’s belief-system. If New Zealand is perfectly happy to receive – into the indefinite future – annual increments of unpaid-for goods and services, and Sweden prefers to keep supplying such stuff without material recompense in foreseeable time, then this sort of unbalanced trade can be categorised as a win-win outcome.

Sweden might not want New Zealand’s (or anybody else’s) debt to it to be repaid; in 2026, or ever. Sweden, happy to run a trade surplus in 2025, might actually prefer to keep making annual ‘gifts’ to New Zealand (and other countries). While each of these gifts would be technically an addition to New Zealand’s debt to Sweden, New Zealand would be able to – maybe, be obliged to – delay settlement of any of that debt (let alone all of it) indefinitely.

In this example, Sweden is a ‘mercantilist’ country; mercantilist means ‘merchant capitalist’, the social science analogue of alchemy. Indeed, Sweden actually is a mercantilist country. Its preference is to accumulate ‘promises’, whereas countries like the United States and New Zealand have been accumulating (and enjoying) imported goods and services.

Mercantilists of yore sought to accumulate ‘treasure’, especially gold. Indeed, in the quarter millennium from 1500 to 1750, economic policy and foreign policy – especially but not only in European power centres – was to become rich by accumulating treasure hoards.

Mercantilism never went away, despite having been debunked by Adam Smith and others around 250 years ago (The Wealth of Nations was published in 1776). In that golden age of mercantilism, the Dutch – the Netherlanders – succeeded par excellence. (Part of their success was in exporting military hardware and software – big guns, and big military knowhow – to all sides in the Thirty Years War of 1618 to 1648. Is that what the USA will end up mimicking?) As we can see from the chart, the Dutch still do incur some of the world’s biggest export surpluses. Instead of accumulating treasure as they did in the seventeenth century – as gold and silver bullion and specie – they now accumulate ‘virtual treasure’ or ‘virtual gold’. Virtual gold is the whole set of ‘promises’ and ‘titles’ – including money and real gold – that are formally known as ‘financial assets’.

New Zealand and America, and others, get the consumable loot. Sweden and Netherlands and Germany get the paperwork. Everyone should be happy.

The dark cloud on the horizon comes when the Americas and the Aotearoas of the world start wanting to be like Germany and Sweden. Then indeed our happyish world descends into a ‘race-to-the-bottom’. Not every country can sit with Germany and its neighbours at the bottom of the above chart. This can be thought of as a see-saw chart: someone has to be at the top; we cannot all be at the bottom.

If some countries have forever-surpluses, other countries must have forever-deficits. Getting to benefit from other countries’ largesse – as New Zealand and America do – may seem like a problem to some. But we should remember that the driving force of the capitalist market system is to want – indeed, to demand – consumable goods and services. Someone has to be able to benefit from all the hard work and sacrifice of others.

*******

Keith Rankin (keith at rankin dot nz), trained as an economic historian, is a retired lecturer in Economics and Statistics. He lives in Auckland, New Zealand.