Source: The Conversation (Au and NZ) – By David Peetz, Laurie Carmichael Distinguished Research Fellow at the Centre for Future Work, and Professor Emeritus, Griffith Business School, Griffith University

Shutterstock

The odds have been shortening on the Reserve Bank of Australia lifting interest again, and Australia’s workers are again being blamed for driving inflation.

Harvey Norman chairman and executive director Gerry Harvey is one of the business leaders flamboyantly warning higher wages will lead businesses to cut staff numbers or increase prices, making it harder for the central bank to get inflation down to its 2–3% target.

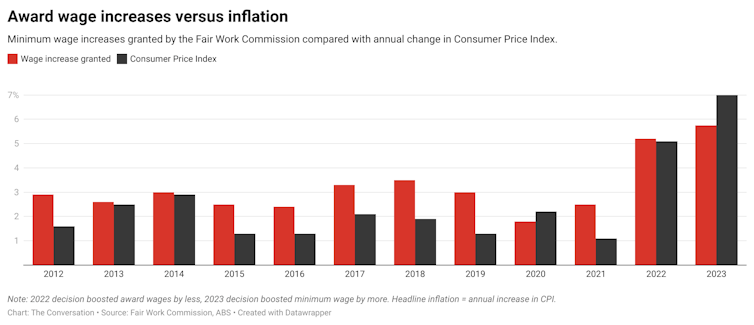

This follows the decision of Australia’s industrial relations umpire in its Annual Wage Review last week. The Fair Work Commission granted a 5.75% increase to award wage rates, and an 8.6% increase to the minimum wage.

But there are good reasons this decision won’t have a material impact on inflation or interest rates.

Limited impact on the wages bill

To start with, the increase in award rates directly affects only about 20% of workers. And those workers, being low paid and often part-timers, only account for about 11% of the national wages bill.

Markets expected a 5% rise anyway. The Fair Work Commission’s decision, being 0.75 of a percentage point above market expectations, means the national wages bill will be only 0.08% (less than one-thousandth) greater than expected.

As a general principle in economics, if the increase in “real wages” (“money wages” minus prices growth) is similar to the trend growth in national productivity, then wage increases will have no impact on inflation.

Over the long run, the Fair Work Commission aims to increase wages in line with growth in prices and productivity. In this decision, though, real wages for even most low-paid workers are falling. Wages growth is putting downward pressure on inflation.

Not all award-reliant workers will get the increase anyway, because there are still employers who ignore awards and underpay employees.

It’s true the decision to increase the federal minimum wage by 8.6% was for more than the increase in award rates. That’s because the minimum wage serves a different purpose to awards. It targets low-wage people who aren’t covered by awards, which is a tiny 0.7% of workers.

The Fair Work Commission raised the minimum wage benchmark from an old, rarely used classification in awards (known as C14) to one matching what most bottom-level workers get paid anyway (known as C13). While the commission is still reviewing the relationship between awards and the minimum wage, this one-off increase, affecting very few workers, is likely to be the biggest change we will see.

À lire aussi :

Up to 1 in 6 recent migrants get less than the minimum wage. Here’s why

What about other workers?

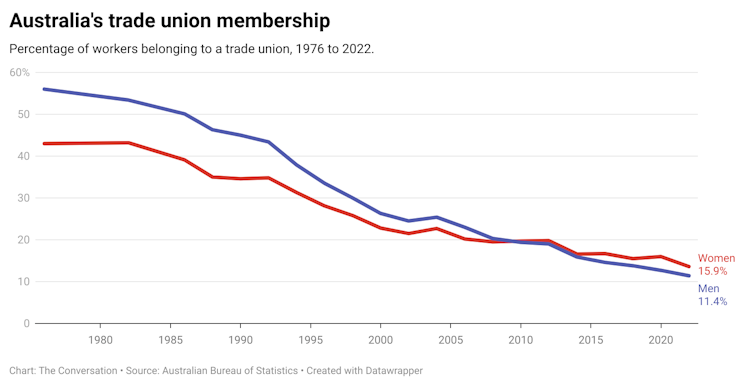

The implications of all this for other workers are very limited. Most workers on enterprise agreements (outside of retail and hospitality) and many on individual contracts receive so much more than the award that an award increase does not matter. Their wage outcomes are more influenced by the state of the labour market, employer approaches to bargaining, inflation and, critically, the bargaining power of unions – something that has been declining substantially in recent decades.

Some workers on enterprise agreements have received such low increases that award rates have caught up to them. This is one reason award coverage has grown from 16% in 2012 to 23% in 2021, but those workers are factored into the cost impact anyway.

With lower bargaining power, average workers’ wages are growing well below prices. There is no way the current inflation can be seen as a wage-price spiral. It is so unlike the last large spike in inflation, in the 1973–74 wage-push period, that any comparison would be laughable.

Reserve Bank governor Philip Lowe in March said “the risk of a prices-wages spiral remains low”. The Bank’s wage forecasts are now slightly lower than then. But by continuing to raise interest rates, it keeps on behaving as if a wages break-out is a real prospect.

À lire aussi :

1970s-style stagflation now playing on central bankers’ minds

Profits and prices

Profits had been growing considerably faster than wages, both in Australia and overseas, though profits are now slowing down in both. There’s a debate in Australia and more explicitly overseas, about the role of profit-making in reinforcing inflation.

Economists overseas have pointed to its likely role after an initial shock, for example from fuel shortages. This includes economists associated with the European Central Bank and the European Commission (so it is no longer a fringe concern).

But firms won’t chase cheap profits through hiking prices indefinitely. Sure, firms have the chance to raise prices more than they need, since customers expect price rises during shortages. Firms expect competitors to match price rises. So they can take advantage of a temporary supply shortage to permanently boost profits. But they’re wary of bumping up prices repeatedly, fearing loss of market share. So inflation (but not prices themselves) should fall.

Indeed, the Reserve Bank of Australia – along with the Treasury and pretty much everyone else – anticipates that inflation is falling anyway. In the central bank’s case, it expects inflation to more than halve, to 3.2% by December next year.

Inflation and interest rates

So there is no reason for the Reserve Bank of Australia to raise interest rates again in light of the award wage decision. It has minimal implications for inflation, which is heading downwards.

That does not mean the central bank won’t raise rates. After all, it increased interest rates last month while inflation was falling. Market expectations of a rate rise were already increasing before the Fair Wage Commission decision, due to a temporary and unexpected rise in monthly inflation figures. If rates rise, it’s not the Fair Work Commission’s handiwork.

À lire aussi :

Lifting the minimum wage isn’t reckless – it’s what low earners need

The problem, as the European Commission’s latest economic forecast warns, is that, when profits and prices rise, workers will seek to offset their loss of purchasing power and income share by raising wage demands. Whether they succeed or not is another matter. But “protracted distributional conflicts could delay the process of disinflation”.

That could affect central bank actions down the track, though effective action on prices themselves would reduce that risk. It also creates policy problems for the federal government, on whether and how to redistribute income back to labour.

![]()

over the years David Peetz has received funding for research from the Australian Research Council, various unions and employers, state and national governments of both political flavours in Australia and overseas, the International Labour Organisation and the Organisation for Economic Cooperation and Development. He is presently employed by the Carmichael Centre at the Centre for Future Work.

– ref. Don’t blame Australia’s lowest-paid workers if interest rates rise again – https://theconversation.com/dont-blame-australias-lowest-paid-workers-if-interest-rates-rise-again-206928