Source: The Conversation (Au and NZ) – By Peter Martin, Visiting Fellow, Crawford School of Public Policy, Australian National University

Reserve Bank Governor Philip Lowe is getting terrible press, most of it undeserved.

“Lowe Blow” and “Take a Hike” were two of the headlines on the front page of one of our newspapers. “We’ve had our Phil” was on the front page of another.

His critics – the ones complaining about continual increases in interest rates – seemed happy enough when he was keeping them low.

Daily Telegraph, August 2, 2022

Lowe and his board are pushing up rates at almost the fastest pace on record, for the same reason they cut them to the lowest level on record – to try to get the economy back into some sort of balance.

It’s tough. But it has been done before, and it worked.In fact, the man who pushed rates down then up even more aggressively than we’re seeing now, former RBA Governor Bernie Fraser, told me this week he approves of the way Lowe is doing his job – with just one exception.

How Lowe’s low rates saved jobs

When COVID hit in 2020, at a time when the Reserve Bank’s cash rate was already a then-record low of 0.75%, the bank cut to what Lowe described as the “effective lower bound” of 0.25%, before cutting again to 0.1%, and offering banks near-free loans at 0.1%.

Lowe’s promise to buy as many government bonds as were needed to push the three-year bond rate down to 0.1% drove three-year fixed-rate mortgages below 2%. Variable-rate mortgages slid to 2.5%.

In concert with the Morrison government, which spent massively in response to COVID, Lowe cut rates to try to keep alive an economy that was shutting down.

Read more:

5 ways the Reserve Bank is going to bat for Australia like never before

The best measure of unemployment is the one that counts as unemployed the Australians working zero hours. It climbed to 15% in April 2020 – the worst since the Great Depression.

The stimulus programs, the arrival of vaccines and the end of lockdowns worked magic, as did the Reserve Bank’s determination to ensure that almost anyone who wanted to borrow could borrow for next to nothing. Spending bounced back, and by July this year unemployment had fallen to a five-decade low of 3.4%.

Then this year inflation – which had remained close to the Reserve Bank’s target of 2-3% for a record 30 years – broke free and climbed; at first to 5%, then to 6% and now 7.3%, all in the space of a few months.

Despite earlier hopes (those who were hopeful in the US and the UK, where this has also happened, called themselves “team transitory”) inflation hasn’t come back down, and shows little sign of returning to 2-3% of its own accord.

Inflation reawakened

Seven per cent inflation matters because an increase in prices of 2-3% per year is very different from an increase of 5-7%. It makes inflation, in the words of former Governor Bernie Fraser, “a subject you don’t discuss at barbecues”.

At 2-3%, people adopt a mental model of fairly steady prices in which, when they agree to provide a service for a certain price, they know what they are getting into.

It’s not so much that high inflation creates winners and losers; the problem is that it becomes almost impossible to tell who those winners and losers will be. It’s the arbitrariness of who does well from timing price increases, and who gets hurt by them, which makes businesses difficult to run and spending difficult to plan.

The RBA’s clear instructions

The Reserve Bank has a written riding instruction from the treasurer to aim to get “inflation between two and three per cent, on average, over time”.

About the only tool it has to achieve that is the manipulation of interest rates.

It is certainly true that much of what set off the latest sudden burst of inflation won’t be restrained by high interest rates. Diesel and petrol prices are set internationally, and soared after Russia invaded Ukraine.

But a lot of what set off and is sustaining the resurgence of inflation most certainly can be tamed by high interest rates.

The rising cost of almost everything

Home building is expensive because of an (internationally-driven) shortage of building materials, and a shortage of workers not laid low by COVID. It is true that more materials and healthier workers would bring down prices, but so too would less demand for building work. Higher interest rates help restrain the demand.

Even the global price of oil can be restrained by high interest rates – not by high interest rate here, but by high rates in the US, which is a big enough nation for consumers tightening their belts to make a difference.

In any event, Australia’s inflation is now incredibly widespread, encompassing almost everything sold here, including most of the things made here.

Ten years ago, 32 of the 87 items priced by the Bureau of Statistics were falling in price, while most of the others climbed. In the latest consumer price update, I counted only six falling in price.

The verdict from a former RBA governor

This week, I rang up the person who’s arguably best qualified to assess the job Lowe’s doing as RBA governor now – someone who was in his shoes three decades ago.

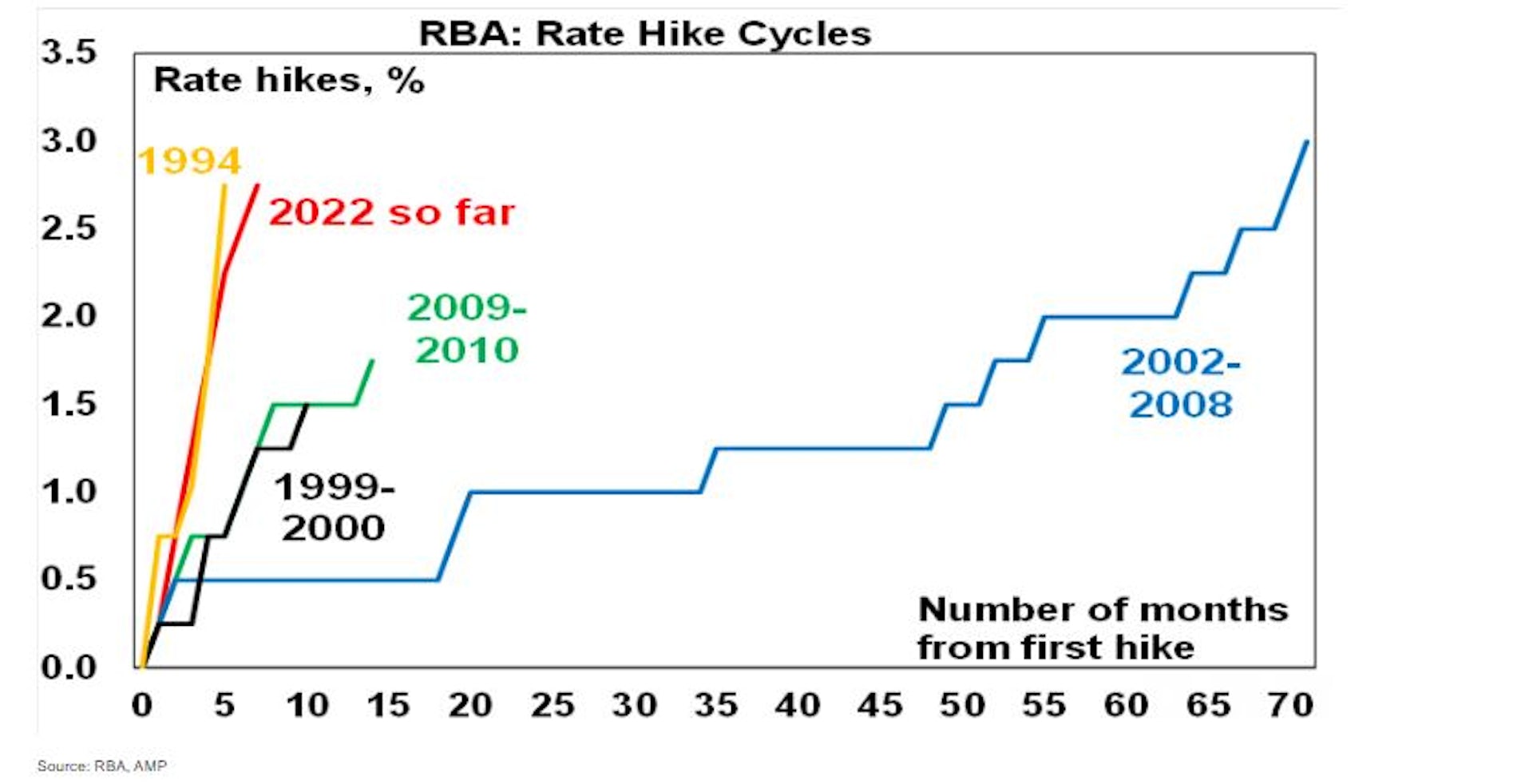

Bernie Fraser was the Reserve Bank’s governor between 1989 and 1996. He pushed down the cash rate 15 times in three years to speed the recovery from the early 1990s recession. Then in 1994, at the first sign of renewed inflation, he pushed them up faster and more aggressively than Lowe has so far this year.

Fraser told me he had wanted to “shock people – let them know that you’re there, that you are concerned about inflation and you want to head it off”.

Read more:

The RBA is hiking rates because it’s scared it can’t contain inflation

Fraser stopped pushing up rates only when he had got inflation down to where it has stayed for most of the past three decades. As it happened, he was able to do it without much pushing up unemployment.

Fraser said he approves of the way Lowe has been doing his job – though he said Lowe was wrong to give the imply during COVID that rates would stay low for three years.

But he also noted setting rates is more art than science.

Fraser thinks that in due course shortages will ease and inflationary pressure will abate. In the meantime, it’s essential to let people know that the bank will do what’s needed to bring inflation down, right up until the point of (but not necessarily including) increasing unemployment.

Fraser thinks there’s a good chance Lowe can bring inflation back down to 2-3%. He should know – he did it before.

![]()

Peter Martin does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

– ref. In defence of RBA Governor Philip Lowe: an easy scapegoat for record interest rate rises – https://theconversation.com/in-defence-of-rba-governor-philip-lowe-an-easy-scapegoat-for-record-interest-rate-rises-194172

{kind=link}

{kind=link}

{kind=link}