Source: The Conversation (Au and NZ) – By John Hawkins, Senior Lecturer, Canberra School of Politics, Economics and Society and NATSEM, University of Canberra

This financial year the Australian government plans to spend at least A$150 billion on so-called tax expenditures – tax concessions or exemptions applying to particular activities or classes of taxpayer.

And that’s just on the top ten tax categories, covering homes, superannuation, trusts, depreciation, food, education and health.

In 2020-21 the cost of these ten tax breaks totalled $118.6 billion. This suggests revenue lost to tax expenditures has climbed 24% in the past financial year.

Commonwealth Treasury

Tax expenditures are spending by another means. Although accounted for in the budget as revenue forgone) rather than revenue spent, they have the same effect as revenue spent on their beneficiaries and on the budget.

Here’s a quick quiz:

-

Are Family Tax Benefits accounted for in the budget as direct spending or revenue forgone?

-

Is the Private Health Insurance Rebate accounted for in the budget as direct spending or revenue forgone?

The answer is it makes no difference. Both of these examples have been classified one way, and then the other. The effect for beneficiaries and the budget is the same.

Optics, however, do make a difference to which accounting measures governments prefer.

Spending attracts attention

Measures on the books labelled as “spending” attract attention. The government’s expenditure review committee tries to keep spending down. Measures labelled “concessions” get less attention, and are seen as a way to keep tax down.

So measures with similar purposes get treated differently. Spending on age pensions gets scrutinised, for example, while superannuation tax concessions become part of the landscape.

If you want government support for your cause or your type of people with minimal attention, therefore, you should get that support classified as a “concession” rather than “spending”.

Tax breaks ‘disguise’ expenditure

The term “tax expenditure” was introduced to Australia by the 1973 report of the review of expenditure policies established by the Whitlam government in 1972.

The review, led by former Reserve Bank of Australia governor H.C. Coombs, had been asked to examine spending but also looked at 48 “disguised” tax expenditures.

Since 1980, major tax expenditures have been included in budget papers. Since 1986, at the behest of then treasurer Paul Keating, the federal treasury has prepared an annual tax expenditures statement.

Read more:

Boosting super will cost the budget more than it saves on age pensions

In 1996 then treasurer Peter Costello made the statement a formal requirement in the Charter of Budget Honesty.

Benefits for the better-off

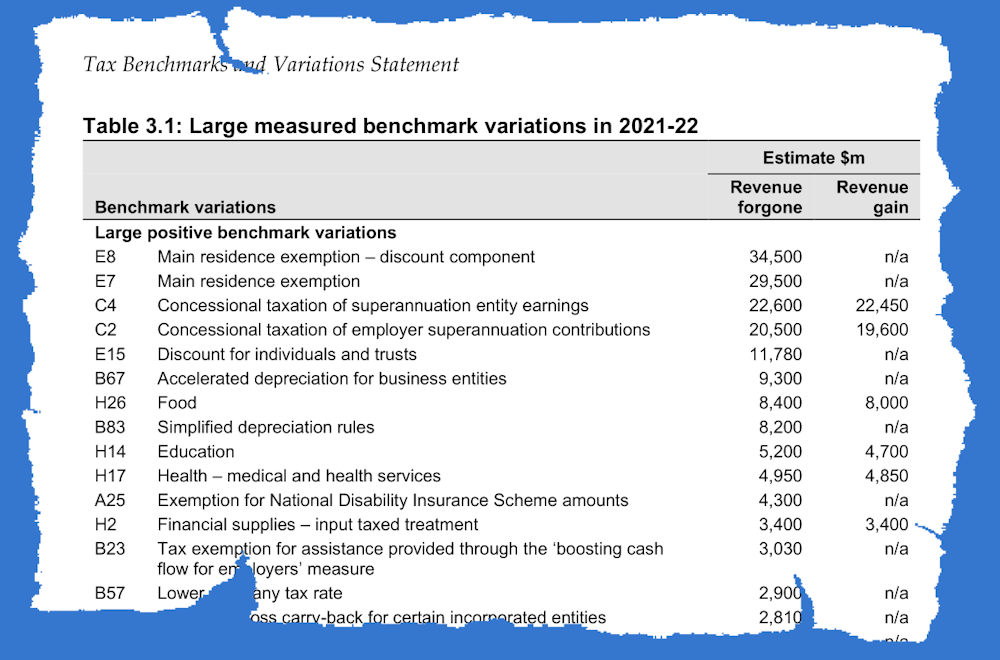

This year (as with most years) the biggest tax expenditures are:

-

exemptions from capital gains tax for private homeowners ($64 billion)

-

tax concessions on superannuation fund earnings ($22.6 billion)

-

tax concessions on superannuation contributions ($20.5 billion)

-

the treatment of only half of each capital gain as taxable ($11.7 billion)

Soaring home prices have pushed up the cost of the homeowner tax concessions 28%, while the stronger share market has pushed up the cost of the concession on superannuation fund earnings 15%.

At least in these two big instances, the biggest tax expenditures go to the most well-off Australians. This isn’t universally the case – the exemption of fresh food from the goods and services tax, for example, disproportionately benefits Australians on low incomes – but generally the more of a tax someone would be liable for, the greater their gain from any concession.

‘Revenue forgone’ versus ‘revenue gain’

The cost of tax concessions has traditionally been described in terms of revenue forgone. But critics make the point this isn’t equal to the revenue that would be gained if the concessions were removed.

shutterstock

It might be (for instance) that people would put their money elsewhere if they knew the capital gains on their homes would be taxed the same way as other assets. It might be that they would put less into superannuation if they knew the returns would be taxed at standard rates.

Partly to reflect these concerns, the name of the “tax expenditures statement” was changed to “tax benchmarks and variations statment” in 2018.

The federal treasury has begun preparing what it calls “revenue gain” estimates alongside “revenue forgone” estimates – an acknowledgement that less will be gained by removing tax breaks than appears to be lost by putting them in place.

For example, the GST exemption for fresh food is said to cost $8.4 billion in forgone revenue, but the treasury estimates only $8 billion would be gained if exemption was removed because some people would switch to prepared food.

Probably the most striking thing about the treasury’s revenue gain estimates is how little they differ from the revenue forgone estimates.

Read more:

Boosting super will cost the budget more than it saves on age pensions

The concessions for superannuation fund earnings, for example, are said to cost $20.5 billion, and the gain from abolishing a similar $19.6 billion. This reflects both the compulsory nature of superannuation and a belief that most Australians who save for retirement will continue to do it, if not through super then through another mechanism that attracts tax.

Tax expenditures tell us a lot about the size of government commitments and what they cost. The Coombs review wanted each limited to three years and then replaced with direct spending that achieved the same effect.

We’ve yet to get a treasurer prepared to embrace that reform.

![]()

John Hawkins was formerly a Treasury officer and served as secretary to the Senate Economics Committee.

– ref. How to camouflage $150 billion in government spending? Call it ‘tax expenditure’ – https://theconversation.com/how-to-camouflage-150-billion-in-government-spending-call-it-tax-expenditure-176236