Source: The Conversation (Au and NZ) – By Ian Marshman, Honorary Principal Fellow, Melbourne Centre for the Study of Higher Education, University of Melbourne

Most of Australia’s universities have adequate cash and investment reserves to deal with the immediate impact of a downturn in international student revenue in 2020. But the longer term prospects are grim.

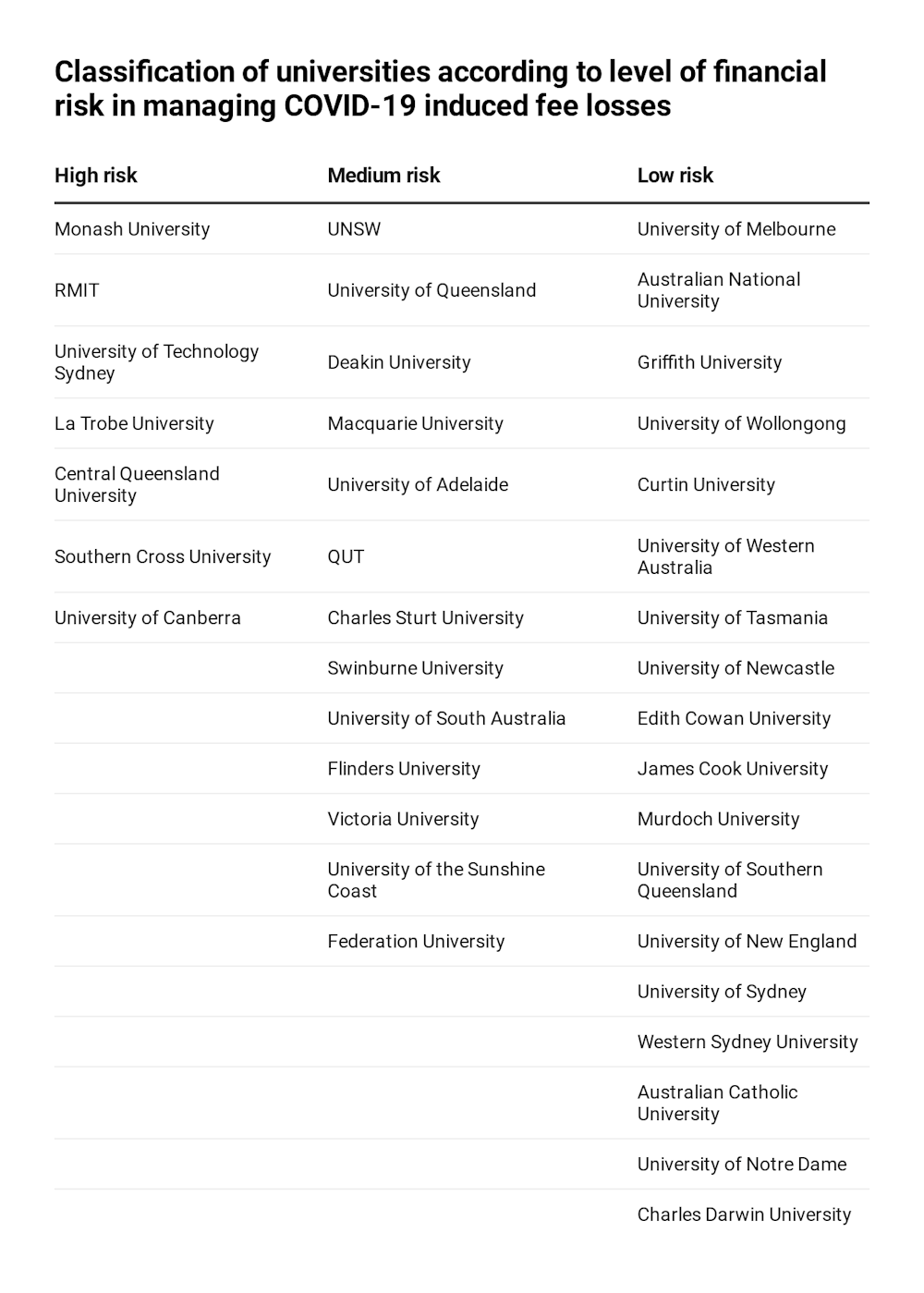

We modelled the impact of the loss of international student fee income resulting from COVID-19. We used 2018 data and categorised 38 Australian universities into three risk categories: high, medium and low.

We found seven universities are most at risk of having their international student revenue losses exceed available cash and investment reserves. These are: Monash University, RMIT, University of Technology Sydney, La Trobe, Central Queensland and Southern Cross University, and The University of Canberra.

The decade from 2009 to 2018 saw Australian universities enjoy an unprecedented boom in international student enrolments. The revenue from this activity increased by 260% – from A$3.4 billion to A$8.8 billion.

This has created significant threats to universities, which became increasingly reliant on international student fee income to fund teaching, research and capital infrastructure programs.

Read more: How universities came to rely on international students

Just four months ago this strategic threat was realised. The most pervasive impact of COVID-19 on Australian university finances will be the loss of international student fee revenue.

Modelling by Universities Australia shows the sector will lose A$16 billion by 2023. This is similar to our predicted losses of international student fee revenue amounting to A$18 billion by 2024.

A critical issue is how well universities are placed to manage this pandemic-induced financial crisis.

Short and long term scenarios

Our study examined the short (for 2020) and longer term (to 2024) impacts of the loss of international student fee revenue.

We assessed the risks using short term and longer term optimistic and pessimistic scenarios.

The optimistic scenario considered overall international student numbers will return to pre-COVID-19 levels by 2024. The pessimistic expected longer term damage to international education.

We used cash and investment reserves to assess universities’ financial resilience. These reserves are the most accessible forms of liquidity available to offset a sudden loss in income.

We determined only a proportion of total cash and investments to be able to offset revenue shortfalls. The proportion increases over the longer term. Universities do have other assets, but most are not readily accessible for alternative deployment.

Read more: Why is the Australian government letting universities suffer?

Seven universities (as cited above) have insufficient available cash and investment reserves to offset predicted losses in international fee revenue for 2020. This is also the case for both the pessimistic and optimistic longer term scenarios.

Of these, Monash University, RMIT and UTS have very large numbers of international enrolments. Revenue from international student fees constitutes 34% for Monash, 36% for RMIT and 35% for UTS. Across the sector international student fee income constituted 26.2% of total revenue in 2018.

For Central Queensland and Southern Cross University, international fee income as a proportion of total revenue is above the sector average – 33% and 27% respectively in 2018.

In absolute terms two of seven universities at most risk – Southern Cross and Canberra – have very low levels of available cash and investment reserves. This that adds to their financial vulnerability.

In the longer term another 13 universities – including the research-intensive UNSW and The University of Queensland, as well as The University of Adelaide, South Australia and Flinders University – face medium financial management risk in having insufficient available reserves to deal with the predicted outcomes for the pessimistic scenario.

The remaining 18 universities, just under half of the total sector institutions, are in the low risk category, but most still face significant financial challenges. All five Western Australian universities are in this category.

Of the large research intensive universities, The University of Melbourne is the only university with sufficient reserves to offset the predicted revenue loss under both short and longer term scenarios.

Given their relative smaller cohorts of international students, the majority of regional universities are predicted to be less exposed financially.

What universities need to do

Few universities have sufficient operating margins or available cash and investment reserves to withstand a sustained reduction in international fee revenue.

Without significant increases in public funding (which is unlikely), each university will, to varying degrees, need to identify and build additional revenue streams, and/or significantly reduce spending.

Universities are actively planning and implementing various strategies to mitigate potential losses. The most important strategies will include:

-

delay or scaling back of uncommitted capital works and other major projects

-

a re-appraisal of infrastructure requirements for a post-COVID-19 environment may realise assets surplus to future needs

-

universities with multiple campuses should conduct a major review of the viability of each in a post-COVID-19 world

-

a rationalisation of course and subject offerings to ensure individual program viability over the longer term

-

a rigorous review of “other expenditure” costs. Possible areas for savings include travel, entertainment, use of consultants and marketing expenses

-

a reappraisal of head office structures and remuneration levels, with a view to consolidate roles which may have emerged in a period of plenty

-

a further review of administrative and professional staff costs which amounted to A$8.6 billion in 2018. Sector-wide benchmarking is already available to assess relative efficiency on a function by function basis

Given employee costs represent 57% of total university spending, further reductions in this area are inevitable to reflect the decline in student enrolments. Each university may also need to adjust its workforce capability to meet changed future requirements.

One unprecedented measure involves university leaders seeking collaboration with unions to modify existing enterprise agreements to allow for a temporary salary freeze. Job losses will nevertheless occur, with casual and fixed term staff most at risk.

At the same time, universities will need to continue investing in digital education and new forms of student experience capable of attracting and retaining both domestic and international market share in a post-COVID-19 era.

COVID-19 will test the resilience of all Australian universities in a manner rarely – if ever – seen before. Not all 38 universities will emerge from the pandemic in their current form.

– ref. COVID-19: what Australian universities can do to recover from the loss of international student fees – https://theconversation.com/covid-19-what-australian-universities-can-do-to-recover-from-the-loss-of-international-student-fees-139759